War in Iran and the Russian Economy

By Lily Donahue | 20 April 2026

Summary

The Russian economy remains afloat - propped up by defence manufacturing, trade with China, and sanctions workarounds - but is untenable. Civilians bear higher tax rates, while elites struggle with mass asset seizures.

The war in Iran has significantly boosted Russian oil revenue, but GDP continues to fall.

Russia is likely to escalate ballistic missile usage to exhaust Ukraine’s American-delivered Patriot stock, while growing U.S. war fatigue may weaken Western aid to Kyiv.

Context

The Russian economy, dulled from its earlier bombast but ever resilient, remains in a uniquely precarious position, although a collapse remains highly unlikely throughout 2026. Though Russia’s economy has been gradually weakening since the start of the war in Ukraine, it has proven remarkably durable - there is little reason to suggest that it will crumple anytime this year, or, indeed, next. Russia’s wartime economy is largely a hodgepodge of financial play: the partial draft combined with exhaustive defence manufacturing has kept financials afloat, with China largely covering the gaps caused by sanctions.

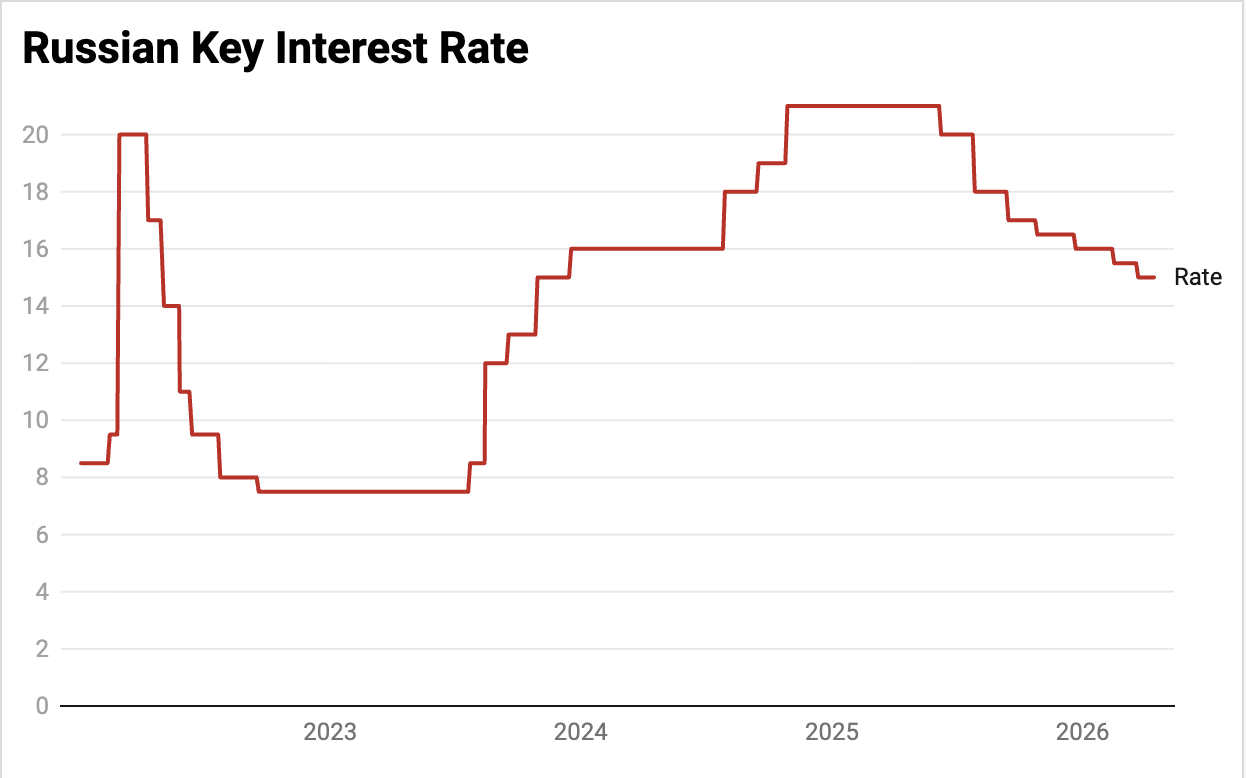

Russian President Vladimir Putin’s economic elites are straining at the bit, but more broadly, the burden of the economy has now fallen squarely on the consumer, with the Russian public now beholden to higher taxes. Key interest rates, which were sky-high at 21% until halfway through last year (now at 15%), have made it difficult for non-war-related businesses to access any meaningful credit. However, popular response remains largely muted due to the highly depoliticised population and maintained support for Putin.

Russia has long been a rentier economy - such rents catalysed the oil boom of two decades ago - but the longevity of such a system is tarnished when the rents relate only to war. Unlike the gas boom, which saw profits redistributed throughout the economy, military rents, inherently, cannot be redistributed. While sanctions have predictably put a wrench in exports, friendly countries have been willing to accept Russian products. With sanctions avoidance, however, come costs: passing through the multiple channels required to hide a Russian origin means that at least 15% of the overall product value is lost.

Alongside this occurs the widespread seizure of oligarchic private property, of which USD 11m was seized in 2025, an increase of 183.5% from 2024. Assets that have not been directly seized have been nationalised, including those of Domodedevo Airport, one of the largest in the country.

Implications

The war in Iran has been lucrative for Russia. It is extraordinarily unlikely to change anything in terms of Putin’s own regime security - no earlier toppling of any Kremlin-friendly despot (Assad, Maduro) has ever proved dangerous for Putin, and will prove beneficial for Russia’s oil revenue. Already, discounts on Russian oil have dropped, providing a welcome respite for Moscow. Urals crude is now selling for USD 117 per barrel, a significant increase from USD 40 in December 2025.

Publicly, however, Putin remains cautious. In remarks to the Russian Union of Industrialists and Entrepreneurs on 26 March - which are rarely made public - the President stated the “consequences of the conflict in the Middle East are still difficult to predict,” and that the war was likely to create conditions similar to those triggered by the COVID-19 pandemic. Putin was reported to have nudged the arranged tycoons into making contributions towards the war effort, a report that Kremlin spokesperson Dmitry Peskov later denied, with the prospects for the Russian economy remaining poor.

While oil revenue has jumped with the increase in price, Russian GDP continues to fall, contracting by 1.8% in the first two months of 2026. Throughout 2025, the economy grew by 1%, down from 4% growth in 2024. Economic Ministry justifications have been predictably contrived: that there was one less day to work in February 2026 than there was in 2025, and this 24-hour discrepancy explains the fall in GDP. Such an explanation, however, does not mention that this schedule was known to the Ministry, and they would have been aware of - and would have accounted for - any such matters.

World Economic Forum/Flickr

Forecast

Short-term (Now - 3 months)

Russia is likely to increase its usage of ballistic missiles, which Ukraine needs US-supplied Patriot interceptors to shoot down, in the hopes this will exhaust Ukrainian supplies.

Russian citizens are likely to become increasingly technologically cut off. Even VPNs, which many liberal-minded Russians rely on to access non-Russian state media, are not foolproof. Crackdowns on VPN usage - to remain in good standing, apps will have to identify users using VPNs - have been announced, set to come into effect on 15 April.

It is highly unlikely that the crackdown on Telegram - though highly unpopular - will push Russia’s disengaged public towards protest.

Medium-term (3 - 12 months)

Ukraine is likely to be increasingly impacted by American war fatigue. With 61% of Americans disapproving of US President Trump’s “handling of the Iran conflict” and even longstanding Trump-allied pundits vocally against the war, it is highly likely this sentiment will influence war aid, allowing isolationist voices to emerge further.

Though the Russian Central Bank cited a stable downward trend in inflation as its reason for lowering the key interest rate, sustained inflation risks remain high.