Thailand's Oil Import Vulnerability: Structural Risks Exposed by Hormuz Crisis

By Jonathan Tenhove | 20 April 2026

Summary

The closure of the Strait of Hormuz on 28 February 2026 reduced Thailand’s oil supply by 50%, causing upheaval in Thailand’s domestic economy, as it appears to have had limited contingency plans for a crisis of this scale.

Thailand will likely go to significant lengths to keep oil prices low, including depleting its strategic reserve, establishing new, expensive procurement sources to meet domestic demand until the Strait of Hormuz is reopened.

It is likely that actions taken to alleviate the Strait of Hormuz crisis will be sufficient in the short term, however, if the conflict continues to escalate, increased domestic oil prices could undermine the fiscal and political credibility of an already fragile coalition government.

Context

On 28 February 2026, the United States (US) and Israel began large-scale targeted strikes on the Iranian military, including the killing of Supreme Leader Ayatollah Ali Khamenei and the destruction of key military infrastructure. These attacks prompted the Iranian navy and coastal defences to close the Strait of Hormuz, through which flows one-fifth of global crude oil.

Thailand has a significant net energy deficit, importing over 900,000 barrels of crude oil per day to meet domestic demand, with around 50% - largely sourced from the United Arab Emirates (UAE) - coming through the Strait of Hormuz. Economic forecasters warn that Thailand will endure a 0.15% GDP hit as oil prices surge, estimating that a USD 10 rise per barrel could push inflation up by 0.5%, increasing the likelihood of economically driven civil unrest.

On 5 March 2026, insurers suspended or cancelled war-risk coverage for vessels transiting Iranian, Israeli, and adjacent Gulf waters, or imposed sharply increased premiums, rendering all crude oil shipments uneconomical. On 11 March 2026, several vessels - including the Thai bulk cargo vessel Mayuree Naree - were hit by unknown projectiles, indicating further escalation with Iran’s intention to suspend passage across the Strait. Additionally, the lack of political willingness from the US, Israel or Iran to end the conflict diplomatically reduces the chance of short-term peace resolution, likely forcing Thailand and other Asia Pacific countries to seek alternative energy suppliers.

Implications

The import-based framework of Thailand’s energy market and the overreliance on Middle Eastern crude oil mean that the root cause of these issues is structural, rather than incidental. The closure of the Strait of Hormuz has prompted Thailand to reconfigure both its international crude oil sourcing strategy and its domestic consumption.

Deputy Permanent Secretary, Veerapat Kiatfuengfoo, claimed that as of 23 February, Thailand had a strategic oil reserve of 4.92b litres of crude and refined oil, which could meet demand for 38 days. Additionally, in-transit stock totalled 2.773b litres from both the Strait of Hormuz and other sources, for a total of 22 days of additional coverage, for a total of 60 days. Statements from government officials in early March suggest that this could be as high as 90 days, given newly established trade partners and forecasting for domestic measures to reduce consumption.

Thailand has also adopted reactive measures to reduce fuel consumption, such as banning exports of refined petroleum products to all countries except Lao and Myanmar, to maintain regional relations. The Thai Ministry of Energy has also instructed coal-fired power plants to operate at maximum capacity, to alleviate the short term reduction in crude oil imports. While these measures prevent a crisis in the short term, they fall short of resolving the broader supply chain disruption. With the diesel cap increase from 29.4 THB (0.9 USD) per litre to 33 (1 USD) on 18 March, popular dissent will likely increase in the short-term, further undermining support for the coalition government formed after the recent election.

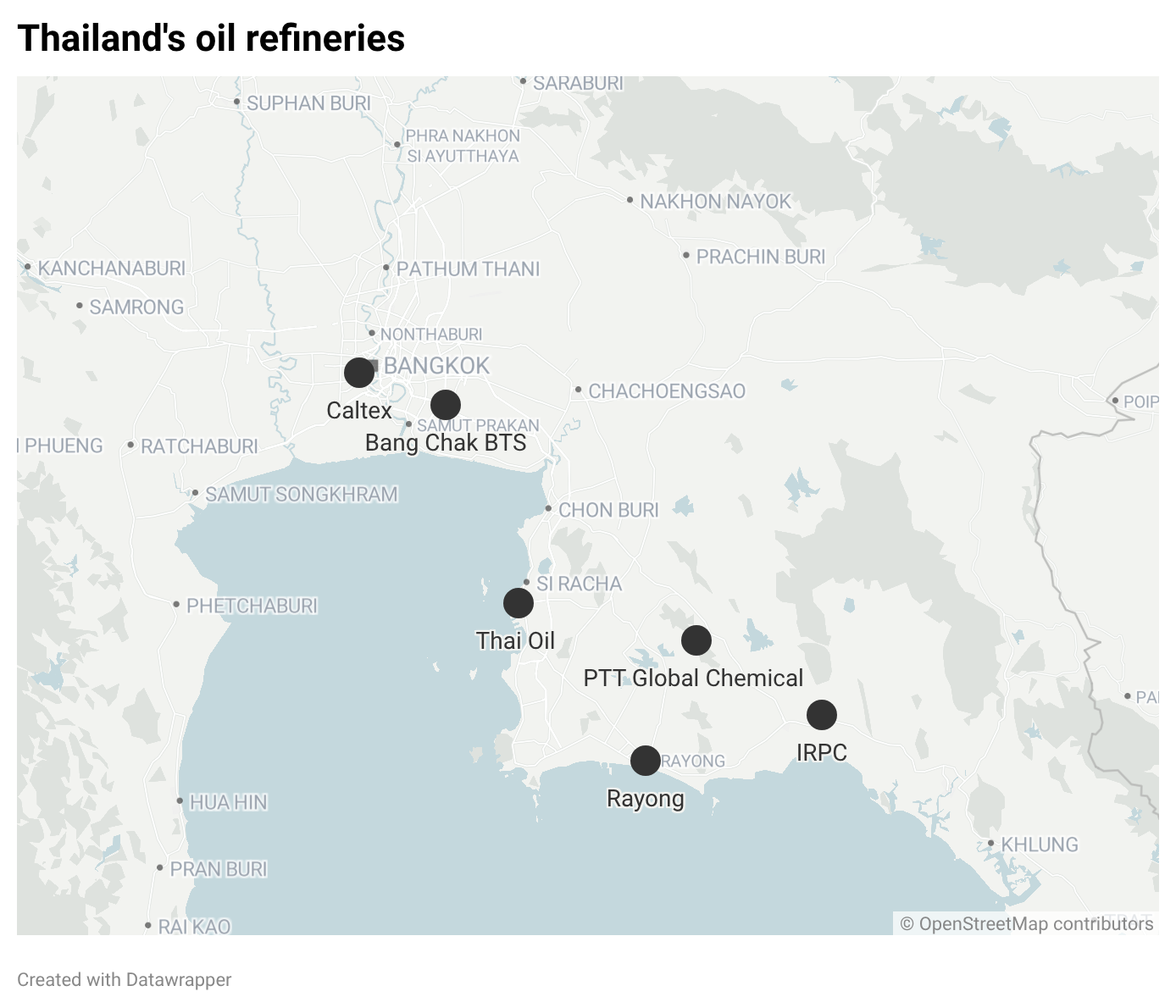

Thailand has initiated the purchase of 1.9m barrels from Angola and 625,000 barrels from the US. While this may bolster the strategic reserve in the short-term, oil procurement from these sources is more expensive due to heightened transportation and insurance costs. Additionally, the low sulphur content of US and Angolan raw crude renders it light, sweet oil and therefore more expensive to purchase than Middle Eastern alternatives, particularly given the increased demand across the globe. While the purity cuts refinement costs, existing Thai infrastructure can refine 1.2m barrels a day, significantly offsetting cost limitations associated with high sulphur oil.

In addition to importing oil from new sources, the Energy Ministry is preparing to raise the mandatory reserve requirement from 1% to 3% to increase domestic stockpiles. This commitment will further reduce available oil stock in the medium-term, likely causing a spike in domestic oil prices. This implies trouble for a fragile coalition government comprised of Prime Minister Anutin Charnvirakul’s Bhumjaithai Party and the Pheu Thai following Thailand’s general elections on 8 February. Failure to handle domestic energy costs could prompt instability. This is viable in the short term while the strategic reserve is still full, however continued subsidy of domestic prices could upend Charnvirakul’s fiscal credibility. Alternatively, failure to do so could diminish his popularity with the broader Thai population.

Farid Mernissi/Wikimedia

Forecast

Short-term (Now - 3 months)

Whether the Iran conflict ends or continues, it is unlikely that there would be a quick recovery to pre-war oil and gas prices. Therefore, Thailand is likely to deplete large amounts of its strategic oil reserves to keep domestic prices stable.

The new commitment to increase the strategic reserve from 1% to 3% will place additional pressure on reducing the domestic oil supply. This will likely cause a major cost increase to domestic consumers, causing some initial unpopularity.

Medium-term (3 - 12 months)

The conflict in Iran is unlikely to end in the medium term, by which point Thailand would have established an extensive network of oil sources at higher procurement costs. Subsequently, domestic oil prices will remain high in the medium term.

Given Charnvirakul’s lose-lose approach to the closure of the Strait, it is likely his domestic popularity will diminish, and his coalition will fracture further, leading to greater political instability.

Long-term (>1 year)

The Iranian conflict is likely to be resolved, or some agreement made to allow the safe passage of civilian vessels to stabilise oil prices. Thailand’s infrastructure and its historic reliance on the Middle East suggest it will revert to purchasing oil at a lower price to maintain demand.

Thai oil companies would have likely met the 3% stockpile goal to be better equipped to deal with a similar crisis in the future, addressing the structural issues within the import-based strategy.