From Adversaries to Partners: Philippines U-turn over South China Sea Claims

By Nicole Pitassi | 20 April 2026

Summary

The closure of the Strait of Hormuz exposed the Philippines as one of Asia’s most structurally vulnerable energy importers, with 95% of fuel sourced from the Middle East. Its negligible domestic production, a transportation sector entirely dependent on imported diesel, and weak fiscal buffers led to a revision in the 2026 GDP growth, bringing it down to 3.7% and an account deficit increasing to 4% of GDP.

President Bongbong Marcos’ signal of openness to joint oil and gas exploration with China in the South China Sea is likely driven by domestic political weakness, as it offers the appearance of decisive action with minimal immediate cost, but a deal that is going to face near-certain constitutional challenge and would provide no short-term energy relief.

The turn toward China weakens the Philippines’ negotiating position on the ASEAN Code of Conduct at a moment when the nation holds the chairmanship, it gives EDCA domestic critics further opportunities against the US alliance structure, and it sets a precedent for China to use energy distress to gain South China Sea concessions.

Context

On 24 March 2026, the Philippines’ President Ferdinand Marcos Jr. declared a state of national energy emergency due to the closure of the Strait of Hormuz, and Marcos signaled the state’s openness to restarting the joint oil and gas exploration talks with China. The statement has taken an opposite course to the position the Philippines’ President has taken since the start of his administration in 2022, resulting in an immediate loss of domestic political support.

The intent comes following the ongoing energy crisis in the Philippines, which import 95% of its oil and gas from the Middle East, while its domestic production remains negligible. The transportation sector uses two-thirds of the nation's fuel and depends entirely on imported diesel. With only one operational refinery, the Philippines has fuel reserves of around 40-45 days.

Fuel prices have doubled since the start of the conflict. ING forecasted the Philippines’ 2026 GDP growth to decrease from 5.2% to 4.5%, and the World Bank forecasted its GDP growth to decrease further at 3.7%. Furthermore, sustained prices above USD 100 per barrel are likely to push the current Philippines’ account deficit from 2.4% of GDP (Q1) to 4% of GDP (Q2), possibly furthering the depreciation of the Peso, currently at the PHP 61: USD 1 mark. Lastly, the unemployment rate has increased from 3.9% in late 2025 to 5.1% as of January 2026, and is expected to rise as energy costs continue to rise.

Implications

The joint exploration proposed by the Philippines’ President will clash with the 1987 Philippine Constitution, which requires the nation to have full control and supervision over natural resource exploration, thereby limiting China's role. Furthermore, the Philippine Supreme Court has voided a tripartite joint seismic survey agreement among the Philippine, Chinese, and Vietnamese state oil firms, ruling that it undermined the Philippines’ sovereign rights over its Exclusive Economic Zone (EEZ). It demonstrates that an arrangement that grants China operational command will likely be overturned by the Filipino Constitution. Therefore, it is likely that the announcement of the reopening of these tals is more a political gesture than a policy proposal.

A turning toward China has a realistic possibility of undermining the Philippines' alliance with the United States (US). Since the start of his administration, Marcos has put effort into deepening the alliance with the US by building 9 Enhanced Defence Cooperation Agreement (EDCA) sites, participating in expanded Balikatan exercises and in the trilateral operation with Japan that placed the Philippines as a frontline partner in the Luzon Strait. Furthermore, Vice President Sara Duterte’s allies have used Iranian missile strikes against US bases in the Gulf to argue that EDCA sites make the Philippines a target, and a joint exploration with China would give further opportunity to call against EDCA sites, which is possible to be viewed by the US as a sign of unreliability.

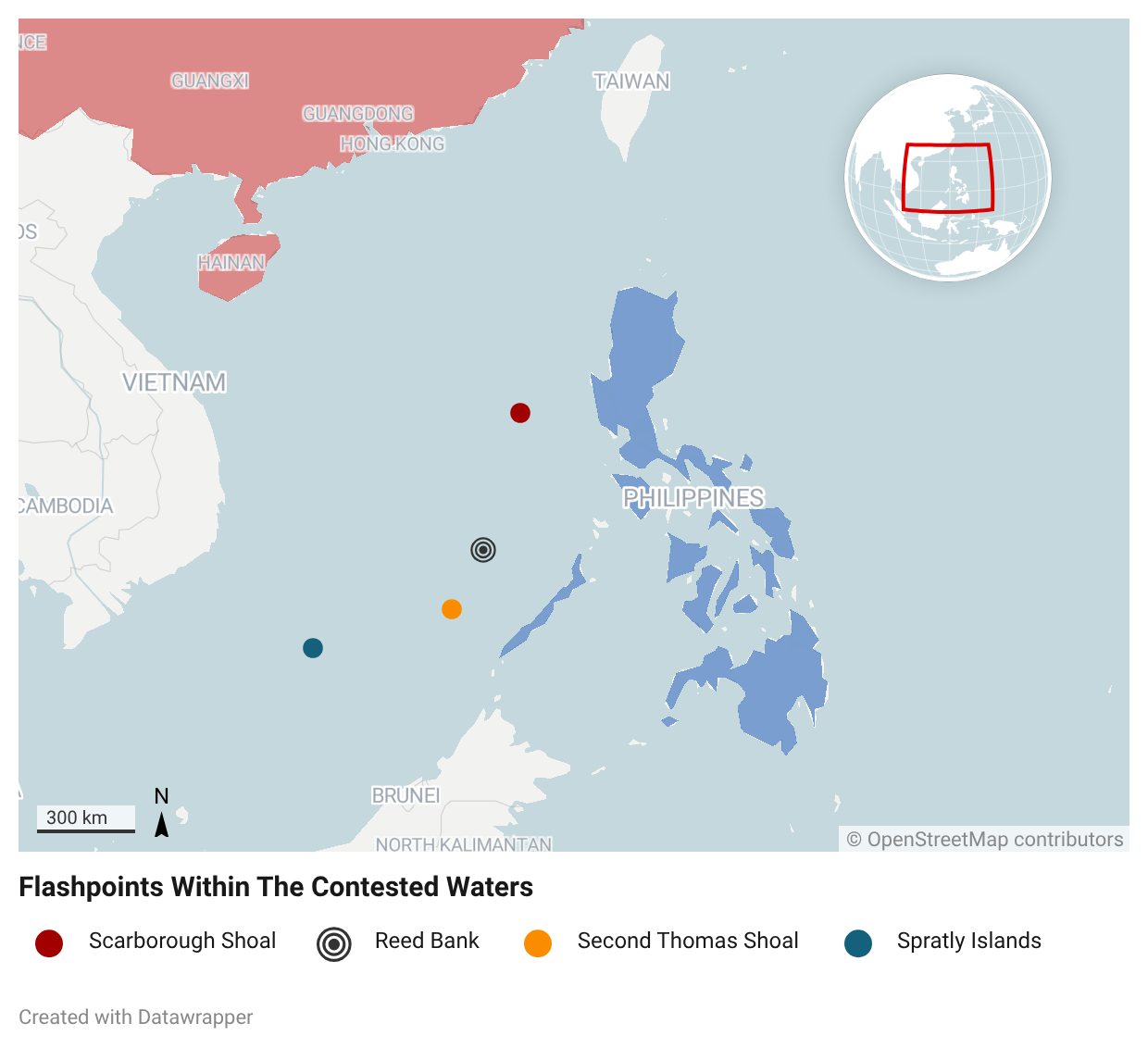

The Philippines is currently holding the Association of Southeast Asian Nations (ASEAN) chairmanship and is tasked with concluding a legally binding South China Sea Code of Conduct (CoC) by July 2026, a role strongly opposed by China. Despite this, President Marcos announced the reopening of joint exploration talks with China, potentially leading to a bilateral energy cooperation outside any multilateral framework, and therefore, undermining the CoC conclusion under the Philippines’ chairmanship and setting a precedent for China to use energy vulnerability to gain sovereignty concessions and replicate it across the region.

The announcement of the reopening of the talks with China as a tool for political narrative diversion is supported by the lack of economic relief that it would bring in the short- and medium-term. The gas produced from Reed Bank would take years to reach operability, and the dependence on Asian refineries, which are themselves reliant on Gulf fuel, would not reduce fuel prices. Moreover, the fundamental structural vulnerability is not addressed by the “policy proposal,” as the transportation sector relies on petroleum, and renewable energy production is currently at 3%.

Despite the joint exploration being a political tool, more than an economic policy, it still has a good likelihood of backfiring. In 2025, a SWS poll found that 75% of Filipinos prefer candidates who believe the Philippines must assert its rights against China’s aggressive actions in the South China Sea. President Marcos entered the current energy crisis amid an ongoing political crisis, due to declining approval ratings, a corruption scandal, and an underperforming economy. Therefore, the joining exploration is a gamble on economic distress overriding deep-seated sovereignty sentiment, and it proves difficult to justify on its merits, and easier to explain as an act of political desperation rather than statecraft.

Forecast

Short-term (Now - 3 months)

Fuel prices will likely remain elevated even with the ceasefire holding, given the Philippines’ dependence on Gulf-reliant Asian refineries. Inflationary pressure on consumer prices is likely to persist through Q2, potentially leading to civil unrest, such as transportation strikes.

Medium-term (3 - 12 months)

The Philippine Supreme Court is highly likely to intervene and block/constrain any joint exploration that will grant China operational access to the South China Sea EEZ.

Marcos’ political position is likely to continue to weaken with increasing pressure from the corruption scandal, energy mismanagement, and a deteriorating economy.

Long-term (>1 year)

The Philippines is highly likely to accelerate and expand renewable energy projects and diversify LNG supply.

The joint exploration proposal will likely drop off as constitutional barriers, military resistance, and a restored energy supply reduce the political incentive behind the reopening of talks.