Red Sea Disruption: Real Cost to African Trade in 2026

By Stephen Nkrumah | 27 April 2026

Summary

Red Sea insecurity is extending end-to-end delivery timelines for trade in East and Southern Africa, as shipments are being diverted and carriers apply tighter restrictions on port access, vessel routing, and cargo bookings.

Import-dependent sectors such as manufacturing, retail, pharmaceuticals, and food processing are likely to face margin pressure due to longer lead times, higher risk-related logistics costs, and increased strain on working capital.

There is a realistic possibility that these rising costs will be passed on to consumers, especially in markets with weak currencies and low inventory buffers, particularly for food inputs and health supply chains.

Context

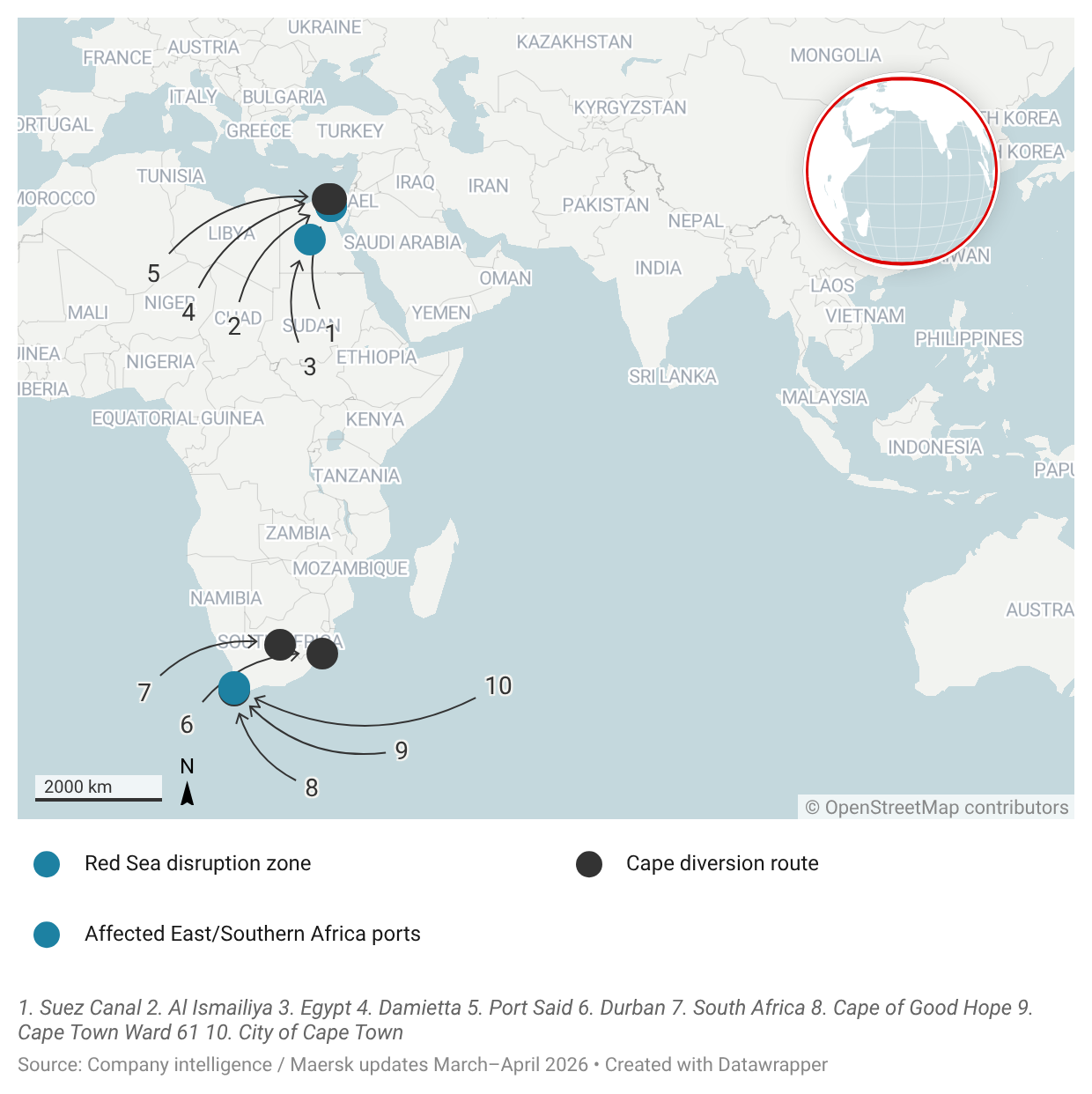

Since late February 2026, renewed insecurity in the Red Sea, which is driven by escalating maritime attacks and geopolitical tensions, has forced major carriers to reroute shipments. This has led to disruption-related surcharges, raising the total landed cost of goods into Africa’s Indian Ocean ports and increasing export costs for time-sensitive cargo. Updates from Maersk in March-April 2026 confirm that contingency routing, surcharges, and some booking restrictions are still in place, showing that the situation continues to affect shipping operations across the region.

The operational impact is clear and measurable. An Africa-focused briefing by UN Trade and Development (UNCTAD) shows that diversions around the Cape of Good Hope usually add more than 10 days to shipping time, increasing delivery delays and putting pressure on firms with limited inventories. The same disruption also raises demand for port services and fuel stops around the Cape, which can lead to congestion and higher risks of delays at Southern Africa ports.

Risk pricing is also increasing. Marine insurance reports and carrier updates show tighter insurance cover and higher war-risk premiums when the route is used, with extra charges reaching about 0.5% to 1% of a vessel’s value during periods of high threat. Maersk has also noted reduced or withdrawn insurance cover for some shipments into affected areas. This can limit routing options and increase costs, even when cargo avoids the most dangerous sections.

Implications

Political risk is becoming more important in the current situation. There is a realistic possibility that governments may introduce ad-hoc trade policy responses, such as temporary tariff or VAT adjustments, tighter import checks, and selective exemptions for essential goods, especially if disruption-driven landed costs continue to rise, and Cape of Good Hope diversions add 10 days or more. It is also likely (60-75%) that public pressure on key inputs like fertiliser and fuel will lead to sudden subsidy changes and slower reimbursement cycles, which can increase counterparty risk for importers, particularly in markets where supply is tight, and import dependence is high, with about 90% of fertiliser in Sub-Saharan Africa being imported. While it is unlikely that maritime disruption alone will cause widespread instability, there is still a realistic possibility of localised protests if shortages of medicines or staple FMCG goods occur.

Economic risk is rising as disruptions continue to affect supply chains. It is highly likely that working-capital costs will increase as lead times get longer, with current re-routing adding about 10–15 extra days compared to the Suez route. These extra days in transit raise inventory financing costs, since capital is tied up for longer. For example, at a 20% annual cost of capital, an additional 10 days in transit adds approximately 0.55% to the cargo value, excluding storage and demurrage costs. It is also likely that margin pressure will be strongest in sectors with limited ability to adjust prices, such as regulated tenders, fixed-price contracts, and highly competitive retail markets. In addition, there is a realistic possibility of faster inflation pass-through where currencies are weak, as exchange rate changes tend to push prices up more quickly, especially in Sub-Saharan Africa, where inflation is already expected to rise in 2026.

Forecast

Short-term (Now - 3 months)

Continued schedule variability and disruption-related surcharges are likely to push up landed costs, with a medium severity, especially for pharma, FMCG, and fertiliser importers on East and Southern Africa routes.

Delivery timelines remain unstable, and higher logistics costs are likely to increase pressure on import-dependent sectors, with a medium severity, affecting pricing, supply planning, and working capital.

Medium-term (3 - 12 months)

There is a realistic probability that prices will pass through more widely, while smaller importers face tighter trade credit as working-capital needs rise and delivery predictability remains weak.

Given this, ongoing delivery uncertainty could push up financing pressure, forcing smaller importers into stricter credit terms and contributing to gradual price increases.

Long-term (>1 year)

It is unlikely that supply chains will adjust over time, with businesses shifting routes and holding more safety stock, which reduces disruption risks but comes with higher operating costs.

Given this, firms may adopt strategies like nearshoring and increased inventory buffers, helping them cope better with disruptions, though at a more expensive cost structure.