Latin America’s Data Center Dilemma: Sold on Renewables, Powered by Fossil Fuels

By Larissa Alves Lozano | 30 March 2026

Summary

Latin America has experienced exponential growth in data center projects due to its abundant renewable energy, primarily hydropower.

Digitalisation and the growth of AI capabilities requiring more data centers have created a power deficit that renewable sources have struggled to address due to their intermittency. This growing gap poses huge financial, environmental, and policy challenges for achieving climate goals in Latin America.

Data centers will continue demanding baseload fossil fuel and nuclear power even as renewable technologies advance. This dichotomy paints a grim picture for balancing climate change mitigation and technological innovation.

Context

In early March 2026, Equinix signed a Power Purchase Agreement (PPA) with Auren Energia to secure wind and solar power for its data centers in Brazil. This is one of many instances of AI and tech companies adapting to Latin America’s energy grid that runs on over 70% on renewables, with growth estimated to skyrocket. In addition to large solar and wind investments across various countries, most of the data center “hotspots” boast of robust hydropower infrastructure and a legacy of fossil fuel generation.

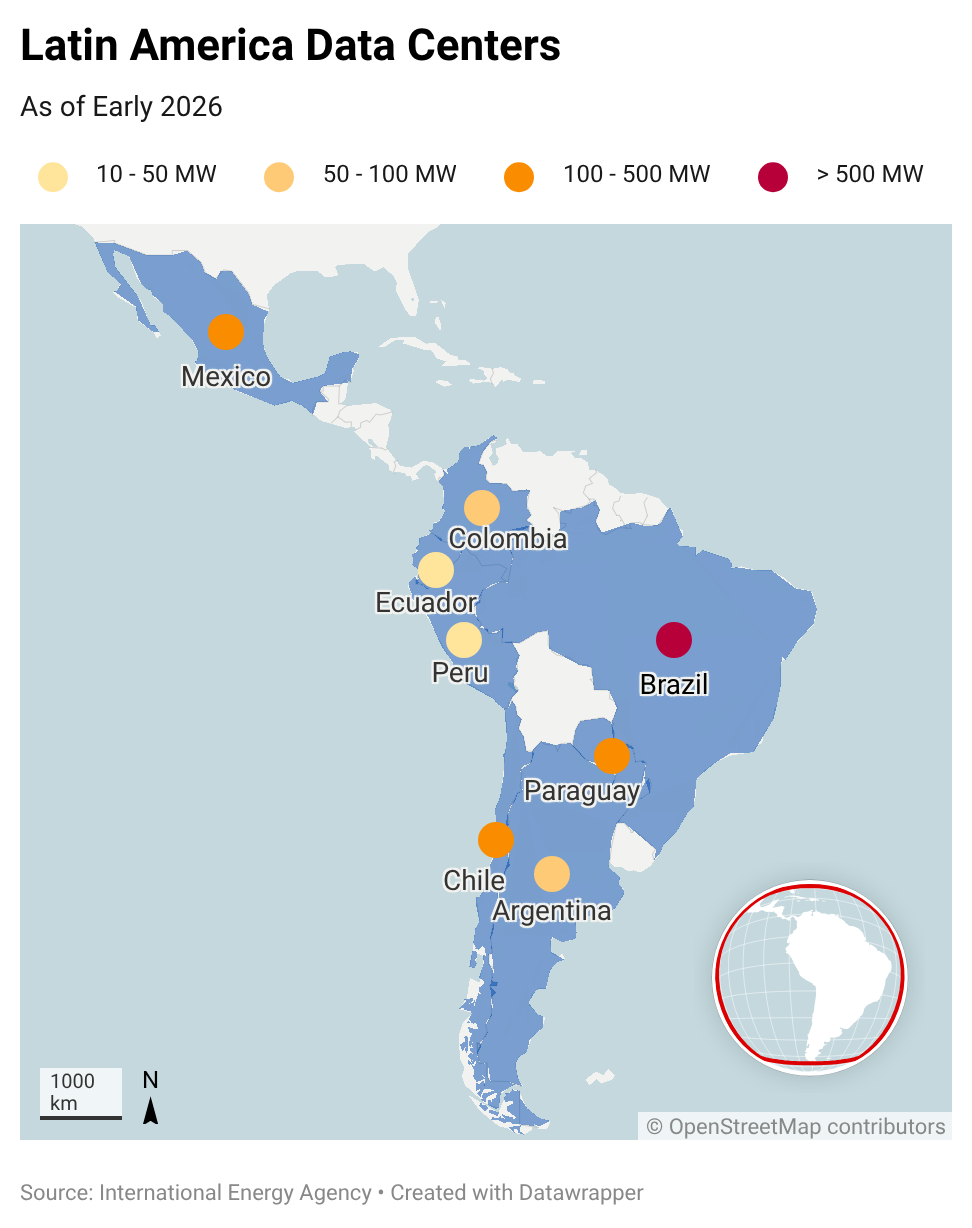

As of 2026, Brazil alone accounts for over 40% of the region’s data center investments, primarily due to local companies such as Ascenty and OData that partner with global players such as Oracle, Amazon, and Meta. Brazil’s electricity mix consists mostly of hydropower (56%), wind (14%), solar (9%), and natural gas (6%). Other notable countries that have notable hydropower generation and have planned data center projects for 2030 include Paraguay (near 100%), Ecuador (72%), Colombia (65%), Peru (48%), Argentina (34%), and Chile (30%).

As North America and Europe turn to nuclear energy as a reliable and environmentally-friendly power source for data centers, Latin America is turning towards wind and solar power, with nuclear power taking a backseat due to high upfront costs.

Implications

The unique focus on hydropower has been a pull factor for large-scale data center projects in Brazil and Paraguay, which share the second-largest hydropower plant in the world with Brazil – Itaipu. It is important to know, however, that Brazil and Paraguay’s model cannot be easily replicated. Hydropower is only viable in regions with sufficient water streams and waterfalls, and differs greatly from wind and solar based on efficiency. Hydropower provides energy at about 90% efficiency (almost all water motion is converted into electricity) and the water gets recirculated through a system of dams and pressurised water channels. Moreover, building dams for large-scale hydro projects takes about 8 years and is extremely resource-intensive (concrete, steel, heavy machinery) and can create environmental disruptions. Not all countries have the geography and infrastructure for hydropower, but wind and solar cannot work alone. Wind turbines have between 20% and 40% efficiency, and solar panels have between 18% and 24% efficiency thus, they need to be supplemented by baseload power generation, which, in Latin America, is mostly fossil fuels.

The dramatic power demand of data centers has re-emphasised the indispensability of coal and natural gas in providing baseload energy in energy portfolios. Renewable energy technologies have greatly evolved in capacity and build quality over the years, but the demand gap remains, as battery storage technologies have yet to reach scale. Even with combined hydropower and wind, solar, and battery storage, renewables cannot provide 24/7 power. That role is fulfilled by either nuclear or natural gas and/or coal.

According to the International Energy Agency, as of 2025, 56% of the electricity consumed by data centers comes from coal and natural gas, and 15% comes from nuclear power. Renewables do comprise about 20% of data center electricity, but they, not even hydropower, can overtake the generation currently fulfilled by fossil fuels. Sunlight and wind speeds increase and decrease over time, while data center demand remains constant and is rising exponentially.

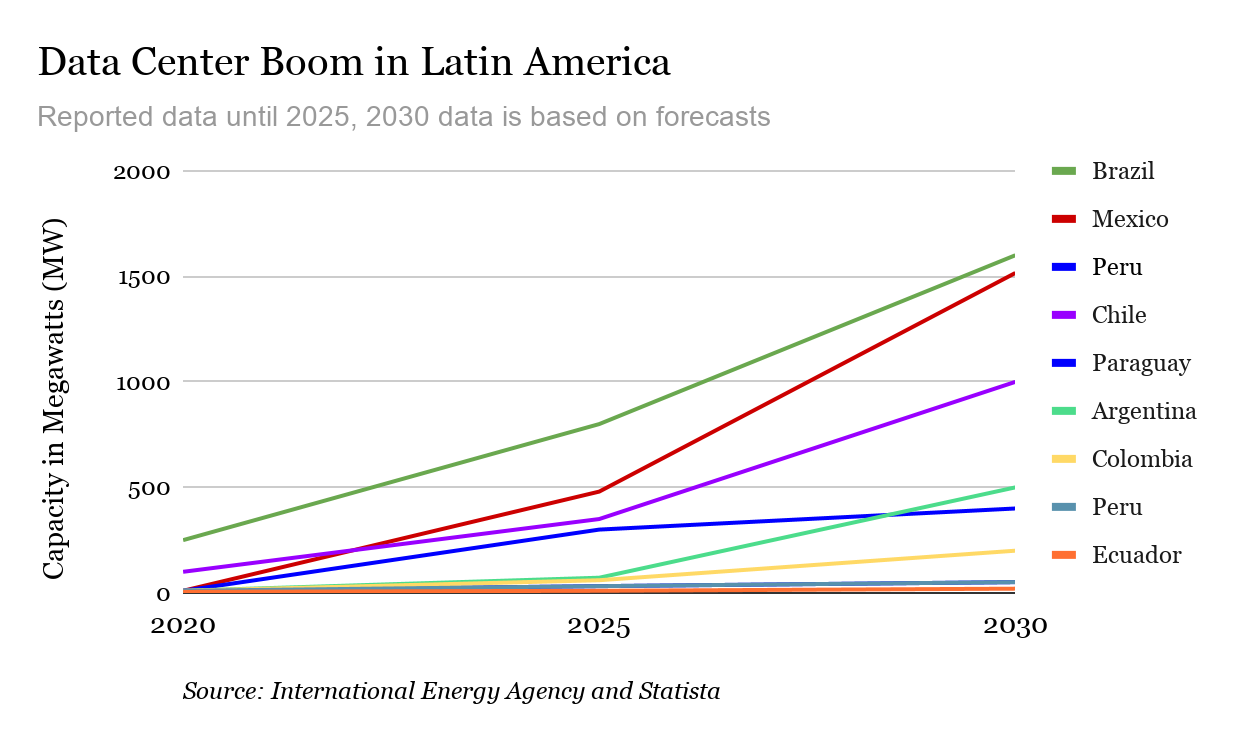

Data center electricity consumption has surged about 15% per year – four times faster than the growth of total electricity consumption across all other sectors (residential, transportation, and industrial). Artificial intelligence development and adoption can further increase this steep increase to up to 30% per year. Moreover, this region already struggles with frequent power outages and crumbling electrical grids, and data centers will further stress power consumption. Nevertheless, the data center industry’s expansion ambitions have not stalled.

2030 data center forecasts seem incompatible with Latin America’s energy transition – higher demand for 24/7 power, but increased intermittent generation. Data centers in Latin America might seem green in theory, but in practice, they are kept afloat by coal and natural gas. Thus, Latin America must choose to fulfil climate goals at the expense of data centers, or develop data centers at the expense of climate objectives. Accepting the role of baseload carbon-emitting fossil fuels is inevitable, but perhaps facing the high upfront costs of carbon-free nuclear power might pay off more in the long-run over wind turbines or solar panels.

Forecast

Short-term (Now - 12 months)

As wind and solar power technologies become more capable and more affordable, it is almost certain that they will remain central for Latin America’s energy transition regardless of data centers.

It is highly likely that data center companies will continue to be attracted to Latin America’s affordable energy and land availability

Long-term (>1 year)

As data centers continue demanding water for cooling, there is a realistic probability that hydropower-reliant countries could see decreased energy generation due to water scarcity.

If companies continue benefiting from cheap electricity and water and lax regulations, there is a realistic possibility for “NIMBY” (not in my backyard) protests against data centers in Latin America.