Indonesia Deepens Resource Nationalism with New Export Agency

By David Yang | 9 June 2026

Summary

Indonesian President Prabowo Subianto has announced plans to establish a state-run export agency through which all exports of certain commodities would be sold, aiming to concentrate the country’s pricing power in commodities where Indonesia holds a large global market share.

In addition to increasing revenues, centralising export sales is intended to reduce under-invoicing and tax evasion and to secure foreign currency reserves to defend the rupiah against depreciation.

The export agency is likely to be most effective in price setting for metals like nickel and tin, where it can complement the government’s downstreaming efforts, while more replaceable commodities like coal and natural rubber would likely see buyers simply shift to plentiful alternatives if they were included in the commodity list.

Context

The Indonesian government has unveiled plans to create a state-owned agency responsible for all export sales of certain commodities in order to further bring Indonesia’s large endowment of natural resources under state control. President Subianto justified the move to clamp down on under-invoicing of export revenues and subsequent tax evasion, and keep foreign currency earnings from exports inside the country to use as reserves to defend Indonesia’s depreciating currency.

Critically for global commodities markets, the centralised agency will negotiate prices with foreign buyers, seeking to leverage the country’s large market share across many industrial, agricultural, and energy commodities to set monopolistic prices and increase export revenues.

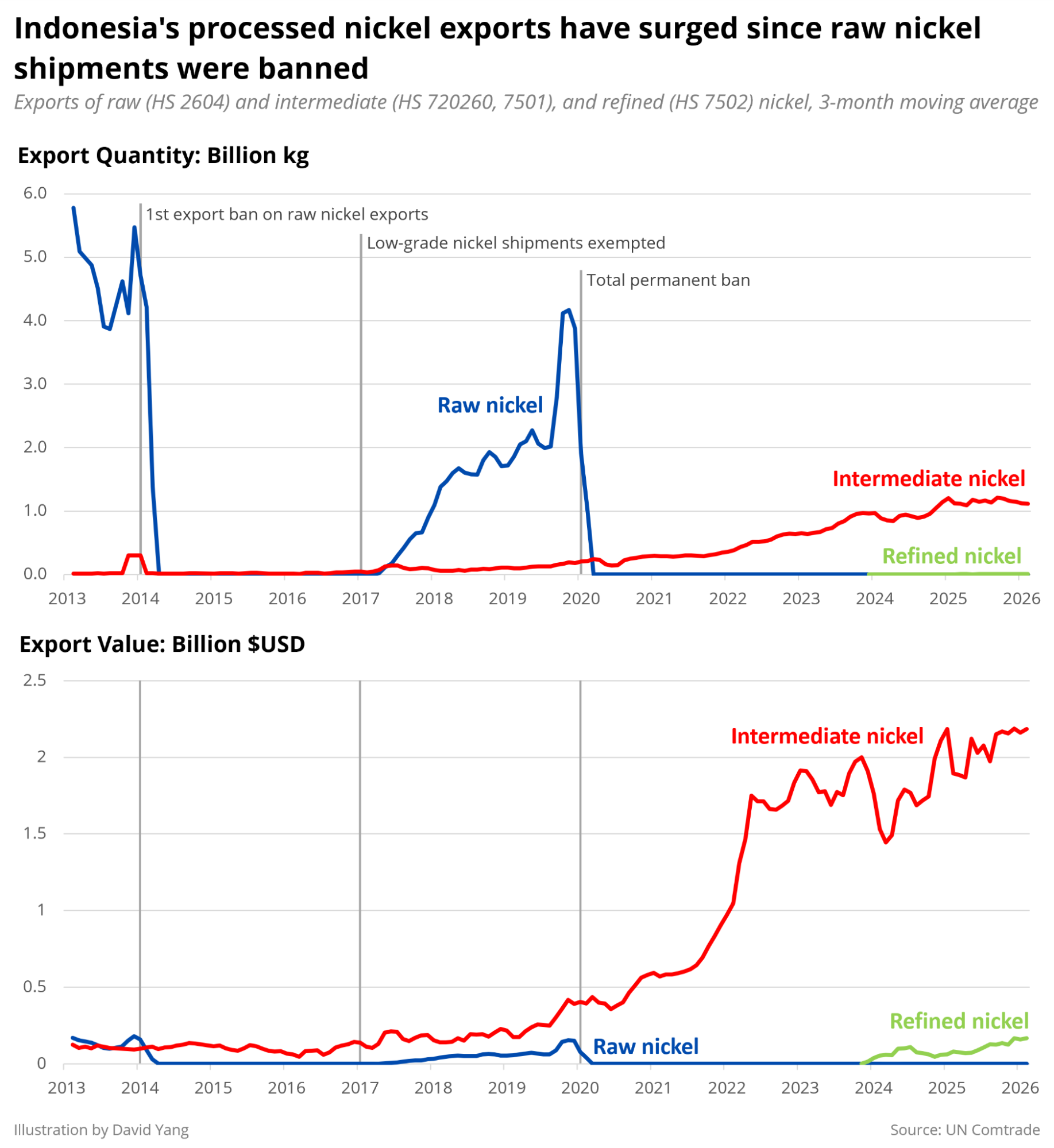

Indonesia has a long history of resource nationalism, seeking to maximise the benefit from its bountiful natural resources, particularly industrial metals. This is most notable with its nickel reserves, the world’s largest at 44% of total reserves. Exports of raw nickel ore were banned first in 2014, then partially exempted in 2017, before being permanently banned in 2020. This forced the development of a domestic refining industry, bringing Indonesian exports down the value chain to more processed outputs at higher prices. The value of processed nickel exports has since far overtaken previous raw ore sales.

Implications

Theoretically, centralising commodity sales under a single government agency should increase Indonesian exporters’ market power, thereby reducing competition among themselves. The country’s large overall share in global commodity export markets provides the bargaining power to raise prices. If Indonesia’s market share is sufficiently large, not all buyers will have alternative sources and will have to accept Indonesia’s higher prices, allowing the country to increase its export revenues for the same level of production.

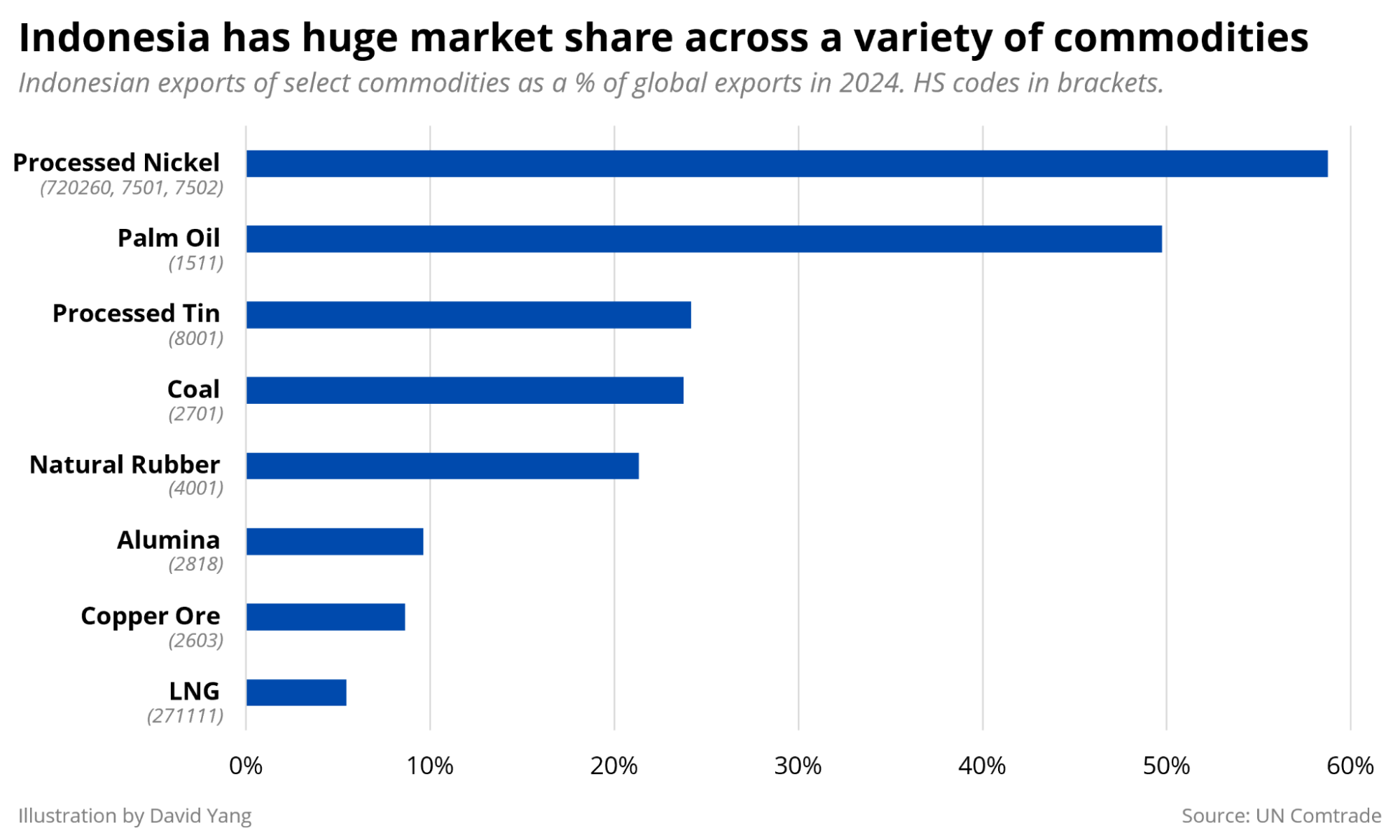

However, the extent to which Indonesia can raise prices without reducing demand for its exports depends heavily on the type of commodity and its alternatives. Despite being the world’s largest exporter of coal and the second-largest exporter of natural rubber, accounting for 24% and 21% of global trade respectively, both commodities are substitutable. Synthetic rubber competes with natural rubber in many use cases, and Thailand still exports over 70% more natural rubber than Indonesia. The world is set to hit peak coal demand before the end of the decade and in light of the closure of the Strait of Hormuz, countries are growing wary of seaborne fossil fuel supply dependencies.

The export agency will highly likely be most effective in its exports of industrial metals. Indonesia dominates global processed nickel exports, and nickel is a necessary material for stainless steel and lithium-ion batteries. Similarly, tin is essentially unsubstitutable in electronic components. What further amplifies the export agency’s effectiveness is how it complements Indonesia’s industrial metal downstreaming efforts. Exports of raw nickel and tin ore were banned in 2014 to develop a domestic intermediate processing industry, but the government hopes to attract further investment into more advanced refined metal production. Raising the cost of its intermediate metal exports incentivises global buyers to invest in Indonesian refineries, just as the export ban of raw nickel created a boom in smelters.

Indonesia’s nickel ban has so far had mixed results in spillovers to the domestic economy. The boom in the domestic smelting industry has increased manufacturing employment, though much of the benefits have been captured by imported specialised labour, with local workers remaining on low wages. Thus, the export agency is unlikely to provide obvious positive short-term benefits to employment.

Global markets did not view the announcement favourably, with S&P Global Ratings warning the plan could choke off government export royalties and negatively impact the balance of payments. This comes on top of investor worries over increased state control in the economy and a widening budget deficit: Fitch and Moody’s ratings have downgraded the country’s credit rating to “negative”, while MSCI is reviewing whether to demote Indonesia from an emerging market to a “frontier” market over transparency and accessibility concerns.

Exact details of the plan remain scarce, with the scheme phased in from June before coming into full force in September. Only palm oil, coal, and ferrous alloys (mostly nickel) will be impacted at first, but the government has stated its intention to review the further inclusion of commodities. However, the government has said it will “listen” to markets and has already clarified to exempt ferronickels (which made up 63% of nickel exports in 2025) and some palm oil derivatives.

J. Zhang , R.F. Singer/Wikimedia

Forecast

Short-term (Now - 3 months)

Market reactions are highly likely to crystallise as the government further clarifies the details of the plan, particularly regarding how existing export contracts will be handled and the extent of margins the government will collect.

Medium-term (3 - 12 months)

Indonesia is unlikely to see a huge increase in its export revenues for commodities like coal, natural rubber, and other smaller commodity exports, as it has far from a monopoly on those markets. Palm oil and nickel, where their market shares are most significant, will be the most likely to benefit from the plan.

Given the phased introduction, impacts on growth and employment are unlikely to be significant in the medium-term.

Long-term (>1 year)

The plan will likely further stimulate Indonesia’s metals downstreaming initiative, bringing more investment into advanced refining of nickel and tin if fully applied to those metals.