China’s Zero-Tariff Policy to Africa

By Yuan Yan | 9 June 2026

Summary

As of May 2026, China has implemented a non-reciprocal, 2-year tariff-free policy covering the majority of Africa (excluding Eswatini).

The policy aims to incentivise economic partnerships, position China as a more open alternative to US protectionism, and isolate Eswatini for its diplomatic ties to Taiwan. While the policy offers African nations significant potential for export growth, investment, and industrialisation, many smaller economies may struggle to overcome infrastructure deficits and stringent regulatory barriers to fully capitalise on these opportunities.

Following an immediate surge in African exports to China, the policy will likely accelerate Chinese investment in Africa and invoke reactions from Washington and Brussels. In the long term, it is likely to drive a transition toward higher-value exports in Africa and intensified regional economic rivalry for the Chinese market and capital.

Context

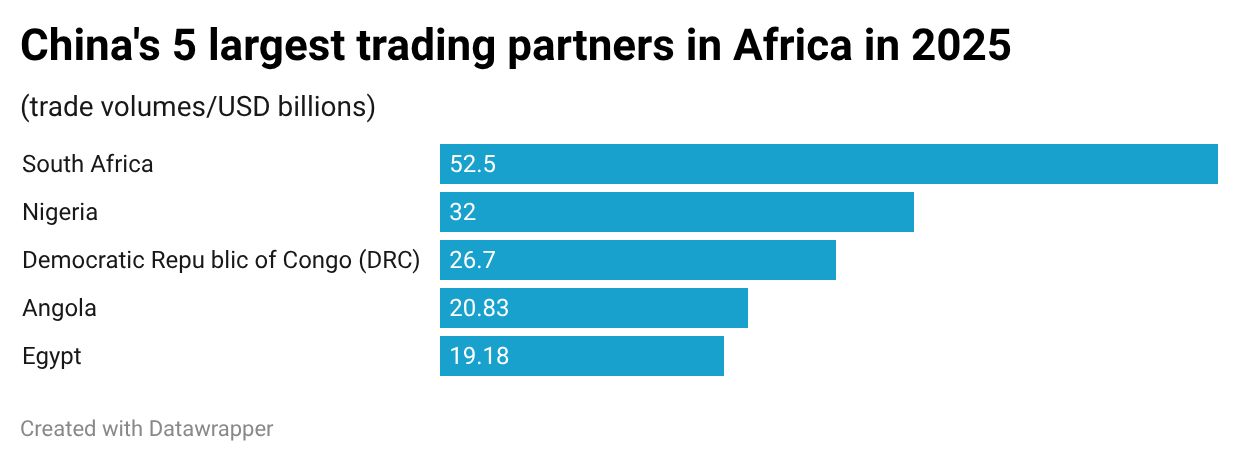

Since surpassing the United States in 2009 to become Africa’s largest trading partner, Beijing has consolidated its economic footprint across the continent. Yet this relationship has also been characterised by a persistent and widening trade imbalance. In 2025, the total trade reached USD 348b, while Africa’s trade deficit widened to a record USD 102b.

On 1 May 2026, China’s tariff-free policy toward 53 African countries took effect. Initially rolled out in December 2024 for 33 least developed countries (LDCs) in Africa, the scheme has since been expanded to include another 20 African states, effective for 2 years until April 2028. As a unilateral move, it requires no reciprocal tariff reductions on Chinese goods from African nations. Shipments of duty-free South African apples and wine, Kenyan avocados, and Egyptian citrus were among the first test cases of this new policy. This new trade access covers almost the entire continent, except for Eswatini, which has diplomatic ties with Taiwan.

Implications

The expansion of zero-tariff treatment serves 3 purposes for Beijing. First, the 2-year implementation period acts as both a temporary buffer and an incentive for ongoing negotiations regarding the China-Africa Economic Partnership for Shared Development (CADEPA), which seeks to institutionalise cooperation in trade, investment, industrialisation, and market access. Second, the initiative allows Beijing to contrast itself with a protectionist United States under the second Trump administration, further establishing the framework for a multi-lateral order by presenting China as the more open, dependable, and pragmatic partner for the Global South. Third, there is Eswatini. As the only African state that recognises Taiwan diplomatically, Beijing deliberately left it out as a form of punishment. This move also narrows Taiwan’s diplomatic space both on the continent and within the Global South.

For African states, the zero-tariff treatment poses both opportunities and challenges. More advanced economies like South Africa and Morocco are highly likely to gain the most from this new trade environment, while LDCs and other less-developed nations will likely struggle to take full advantage of this opportunity due to limited infrastructure and production capacity. Agricultural exporters also face stringent sanitary and phytosanitary standards imposed by Chinese customs, and non-agricultural exporters similarly confront unfamiliar regulatory systems and compliance obligations that may prove difficult, particularly for SMEs that lack the financial resources and technical expertise.

That said, there is a realistic possibility for export expansion for large corporations in the wine industry and agricultural sectors, such as citrus, avocados, and apples, and the lower barriers to entry into the Chinese market mean small and medium-sized enterprises (SMEs) can improve profit margins and compete more effectively. Furthermore, the new trade access will incentivise some African nations to move up the value chain from raw-material exports to branded, packaged, and niche-market products tailored to Chinese consumer demand. Finally, the policy will likely attract more Chinese investment to establish factories in Africa and to export manufactured goods back to Chinese and third-country markets, thus creating more jobs and improving local infrastructure.

Forecast

Short-term (Now - 3 months)

African nations’ exports to China are almost certain to surge, especially their agricultural products.

Medium-term (3 - 12 months)

The negotiations for the China-Africa Economic Partnership for Shared Development (CADEPA) are likely to accelerate, with more bilateral agreements being signed between China and African states.

Exports from Africa to China are likely to continue increasing, and more Chinese capital is expected to flow into African states to establish manufacturing hubs.

There is a realistic possibility that Washington and Brussels will feel pressure from China’s ever-closer engagement with Africa, thus taking new measures to consolidate their economic footprints on the continent.

Long-term (>1 year)

Some LDCs or African states with limited production capacities are likely to experience a slight decrease in their exports to China after the initial surge.

African states with overlapping agricultural exports will likely compete against one another for the Chinese market. Meanwhile, countries with similar manufacturing conditions will also compete for Chinese investment.

There is a realistic possibility that the export profiles of certain African states will evolve, shifting from unprocessed commodities (e.g., crude oil, iron ore, minerals, and coal) to higher-value products.