From Border Disputes to Trade Opportunities: the Economic Implications of the Afghanistan-Pakistan Escalation

By Nicole Pitassi | 16 March 2026

Summary

In early February 2026, multiple suicide bombings in Pakistan triggered Pakistani cross-border airstrikes targeting TTP and ISIS-K camps in Afghanistan. Taliban authorities announced retaliation.

The conflict remains concentrated along critical trade crossings that link South and Central Asia. Closure and insecurity have disrupted supply chains, increased shortages of essential goods, and raised inflation. Pakistan is facing increasing investor pressure from China, while Afghanistan is seeking further trading with Central Asian countries.

Partial stabilisation and renewed escalation are both realistic possibilities. While border crossings could stay open and allow limited trade, militant attacks and retaliations are likely to continue, with Pakistan maintaining its counter-terrorism stance and Afghanistan deepening its economic engagement with Central Asian countries.

Context

The rise in fire exchanges and militant attacks between Pakistan and Afghanistan dates back to 2021, when the United States withdrew its military forces from Afghanistan, leading to the Taliban’s return to power. According to Reuters, militant attacks in Pakistan increased from 658 in 2022 to 2,425 in 2025. Tensions have focused on disputes over the sovereignty of the Durand Line, and they are largely driven by Pakistan’s accusations that the Afghan Taliban has maintained close ties with the Tehrik-e Taliban Pakistan (TTP), a jihadist militant group that targets the Pakistani state, while Taliban leadership is increasingly seeking greater independence from Pakistani influence.

In 2025, tensions further escalated through an increase in both militant attacks and border clashes, which led to the closure of key crossings, including Torkham and Chaman, and therefore the disruption of trade and transit between the two countries. During October 2025, negotiations mediated by Qatar resulted in a brief and strained ceasefire, unravelling in November 2025 after negotiations failed to produce a long-term agreement. Cross-border strikes and retaliatory attacks resumed. In early 2026, multiple suicide bombings took place in Pakistan, with the latest major bombing being a mass suicide attack at a Shi’ite mosque in Islamabad. After blaming militants operating from the Afghan territory for the recent attacks, Pakistan retaliated with cross-border airstrikes on February 21-22, which targeted seven camps linked to TTP and Islamic State Khorasan Province (ISIS-K) in Afghan territory. Since then, the two countries have been retaliating against each other’s attacks, mainly focusing along the border, but also reaching Kabul.

Implications

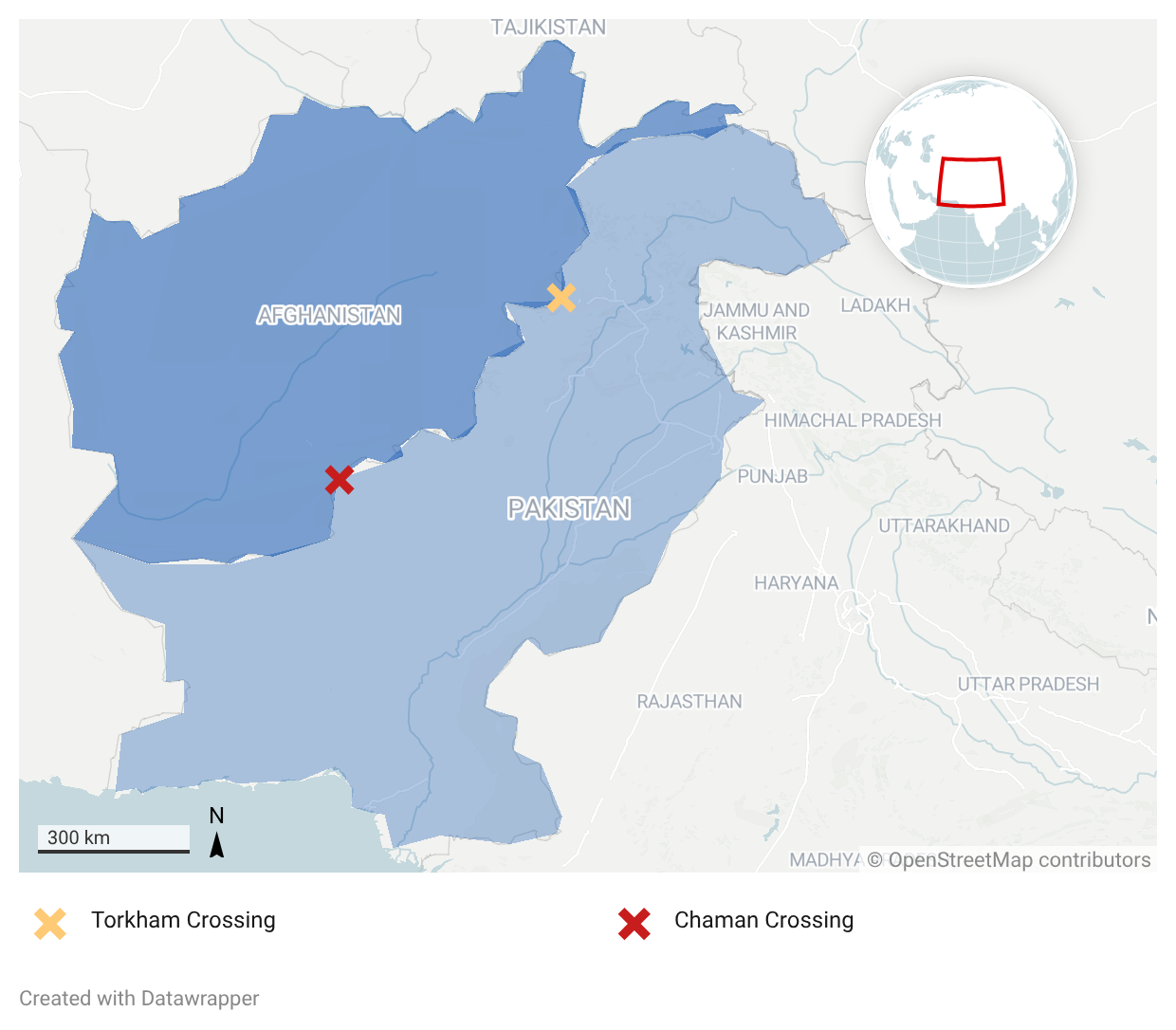

The majority of the skirmishes and attacks occurred along the Pakistan-Afghanistan border, especially near the Khyber Pass, which leads to the Torkham crossing, and at Chaman crossing, both primary trade arteries connecting the two countries and the central Asian region to South Asian ports. The closure of the crossings and the insecurity along these passages disrupted cross-border supply chains, stopping transit flows and delaying humanitarian and commercial supplies. Specifically, bilateral trade dropped from $2.46b in 2024 to $1.77b in 2025, and according to Pakistan’s Central Bank, Pakistan’s exports to Afghanistan fell by 56% in early 2026. Pakistan’s exports lose, on average, $177m per month when the crossings are closed. In October 2025, 5,000 containers carrying goods were reported stranded at the border; these disruptions are driving up food prices. By October 2025, tomatoes had risen by more than 400% in Pakistan.

The two countries differ in strategic positions. Pakistan’s border insecurity and existing internal instability are rising security costs and undermining investor confidence. This brings pressure from China, which has invested heavily in infrastructure through the China-Pakistan Economic Corridor (CPEC). The country is pushing Pakistan to strengthen the protection for Chinese nationals or allow Chinese involvement in Pakistani security arrangements. Since 2005, the Chinese investment is estimated at $62-65b, 74% of which are energy projects. By 2025, China will have signed further project agreements of $8.5b that cover agriculture, industry, and energy sectors.

Afghanistan is redirecting trade toward Central Asian countries to mitigate the border instability with Pakistan. Afghan exports to Central Asian states increased from $122m in 2024 to $216m in 2025. Uzbekistan and Kazakhstan are the major Central Asian countries trading with Afghanistan, with trades amounting to $1.1b and $545m, respectively.

While this decision reduces dependence on Pakistani transit routes, it still leads the country to rely on less developed and costlier crossings. Nevertheless, the decision aligns with Afghanistan’s interest to stabilise transit routes and attract foreign investment. China, as one of the main external investors in Afghan infrastructure and mining projects, is further reinforcing the incentives to stabilize the overall territory, as Afghanistan has the potential to position itself as a transit link between Central Asia, South Asia, and even Europe, as the proposed Uzbekistan-Afghanistan-Pakistan railway would reduce cargo delivery times between Central Asia and Pakistan ports from 35 days to 3-5 days.

Forecast

Short-term (Now - 3 months)

While both sides have incentives to avoid full-scale escalation, tactical military responses and retaliatory actions will likely continue, particularly following the latest high-casualty militant attacks. It is likely that there will be continued low-to-mid-intensity violence and instability along the Pakistan-Afghanistan border, which will lead to intermittent closures or restrictions at key border crossings, disrupting trade flows and supply routes. It is a realistic possibility that India will use the recent escalation to reinforce its narrative of Pakistan struggling to control militant groups operating within its territory.

Medium-term (3 - 12 months)

Pakistan is likely to continue its counter-terrorism measures and cross-border pressure, while it is almost certain that Afghanistan will continue its economic engagement with Central Asian countries to reduce dependence on Pakistani routes. Despite security tensions, economic necessity will likely push both countries to maintain limited trade flows, and China is likely to push Pakistan for an expansion in security coordination around CPEC infrastructure and Chinese personnel.

Long-term (>1 year)

Over the next two years, it is likely that the two countries will fall under a managed instability with selective trade and recurring border tensions, driven mainly by mutual accusations regarding militant safe havens. It is also highly likely that China will strengthen its role as a stabilising partner for Pakistan if the instability threatens major CPEC infrastructure.