Economic Impact of the Iran Conflict in South Asia

By Chongtham Sen Chanu | 10 April 2026

Summary

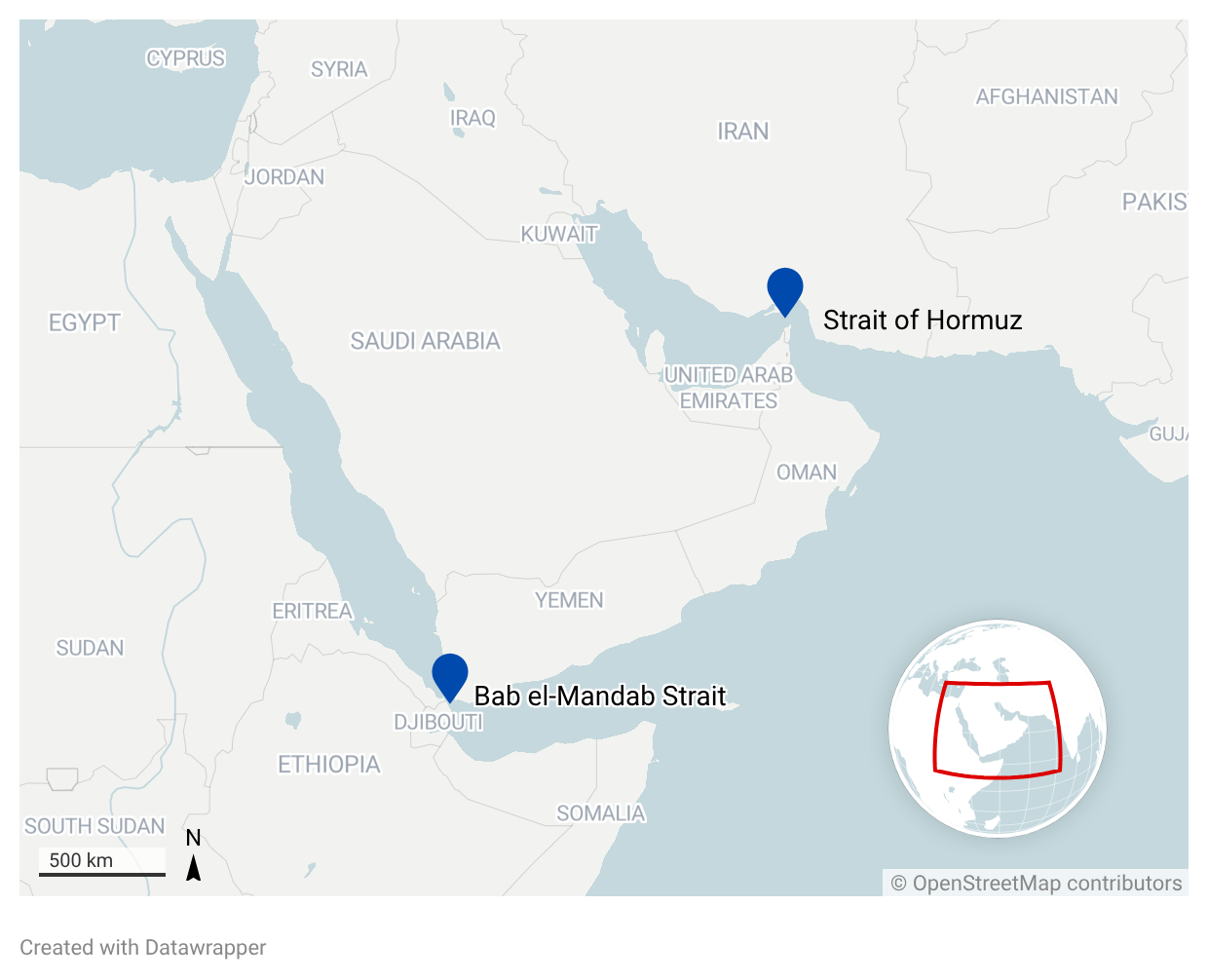

South Asian countries rely heavily on the Strait of Hormuz for their energy imports from the Gulf. The Israel-Iran conflict has caused a shortage of energy supplies and fertilisers, affecting energy-dependent industries.

The current trajectory of the region suggests that a prolonged government subsidy during the oil crisis will likely impact long-term government plans, especially for Bangladesh, further lowering the tax-to-GDP ratio and GDP growth.

Over the next 3 months, increasing fuel prices will likely continue to affect local farmers in the region. There is a highly likely scenario for civil unrest stemming from expensive diesel prices, organised by different farmer associations across the region.

Context

The supply chain disruption of oil and LNG caused by the Strait of Hormuz blockade has increased the threat of inflation across sectors of South Asia’s economy, especially in transportation and agriculture, with agriculture accounting for a significant share of GDP in most countries in the region. The blockade has led to a hike in fuel prices across South Asia, raising the cost of crop harvesting and the transportation of produce to markets. In addition, the Middle East exports a significant amount of fertilisers to the South Asian countries, especially urea and diammonium phosphate (DAP). The conflict disrupted the fertiliser supply chain and caused a roughly 50% price hike in urea. The current conflict scenario indicates that the region’s energy and food security will continue to be affected, with the severity varying by country.

Implications

India

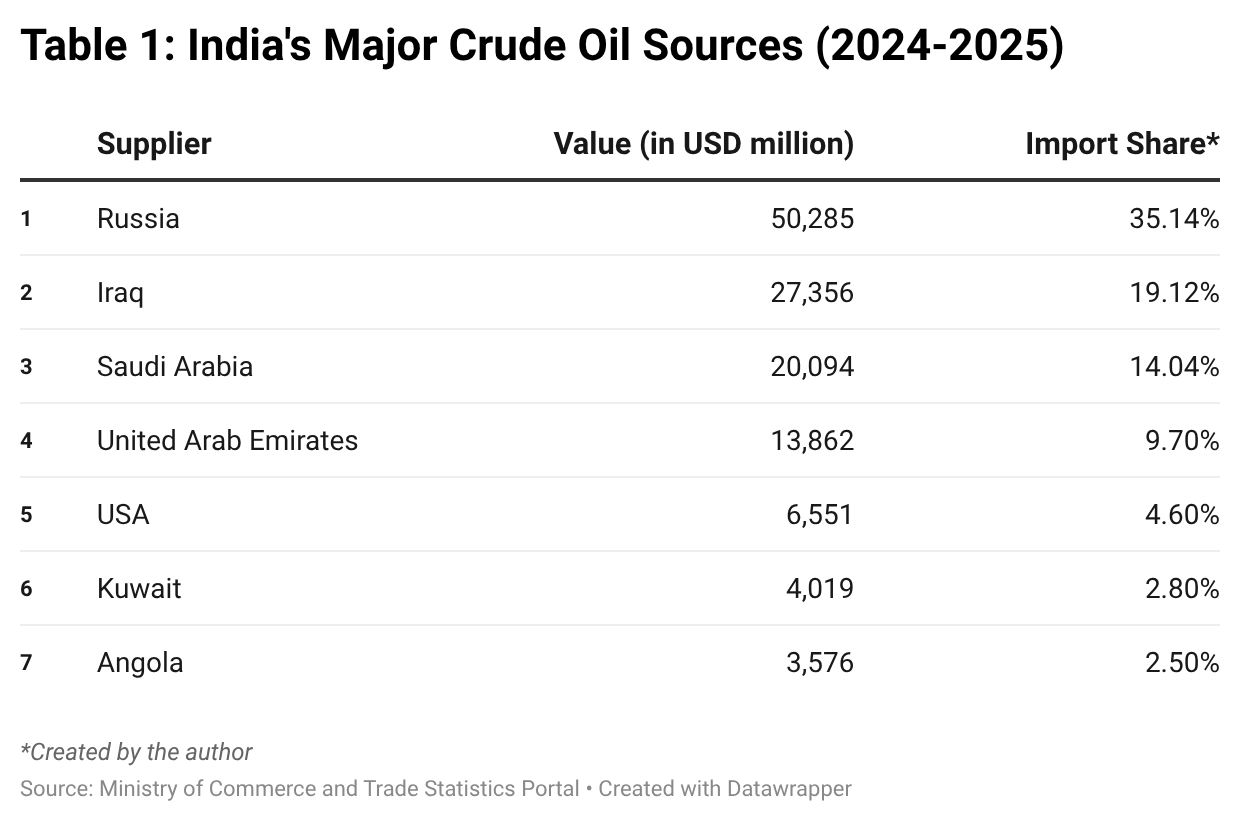

India’s crude oil imports are primarily transported via the Strait of Hormuz (from Middle Eastern countries), the Bab el-Mandab Strait (from Russia and the US), and the Indian Ocean (from African countries). Since the Strait of Hormuz accounts for 40–50% of India’s crude imports, a prolonged closure would slow production growth in energy-intensive industries, such as the automotive and aviation sectors. The government has also prioritised LPG (produced during crude oil refining) for household needs over industrial needs. A weakened automotive industry will likely lower demand for raw materials such as steel, aluminium, rubber, and other components, and a realistic possibility of production line shutdowns due to weaker consumption.

The Indian government stated that the country has 60 days and 30 days supply of oil and LPG. Additionally, it reassured the farmers that the fertilisers are secured to last until the Kharif season (June-October). However, an immediate LPG shortage and inflation stemming from logistics disruptions resulted in production delays and temporary shutdowns for small and medium-sized enterprises (SMEs). Although the government has partially exempted customs duty for petrochemicals to stabilise the domestic supply, the looming threat by the Houthis to close the Bab el-Mandab Strait remains a destabilising factor. India’s trade with the US and the European countries, exceeding GBP 245b (USD 325b) in FY25, is routed through the Bab el-Mandab Strait–accounting 20% of the country’s total trade. A blockade of this strait will almost certainly further undermine India’s electrical industry and other pharmaceutical exports.

Pakistan

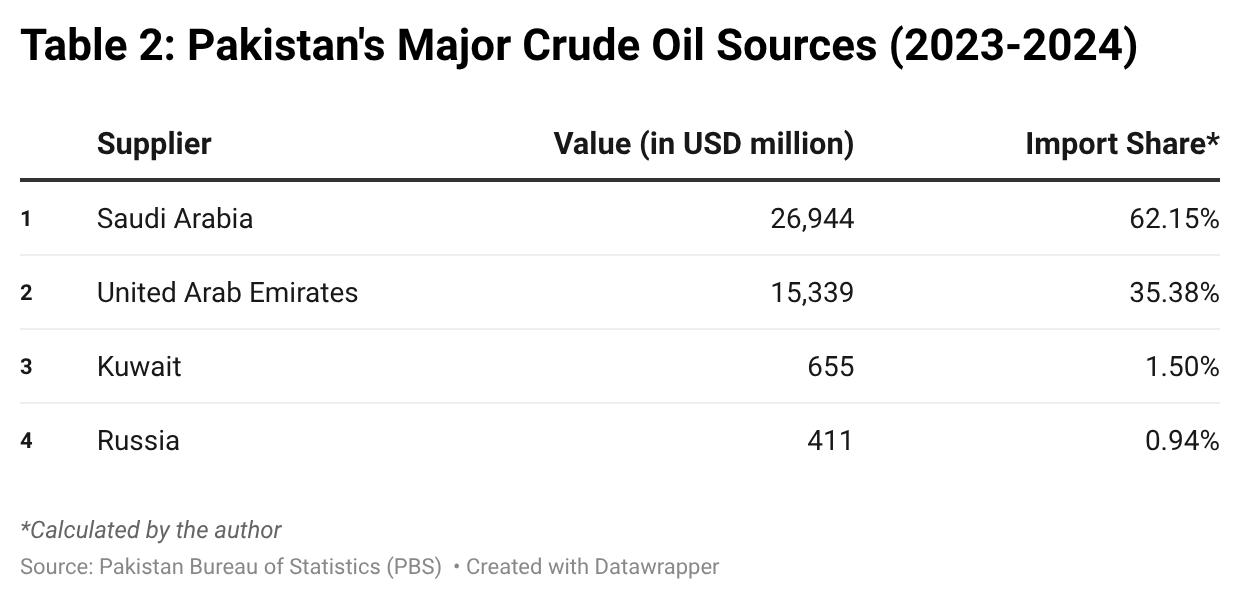

Pakistan increased the price of petrol and high-speed diesel by PKR 378 (USD 1.35) and PKR 520 (USD 1.86). Pakistan is highly dependent on the Gulf countries for its energy imports (as shown in Table 2). Although agricultural products will become more expensive due to increased production costs, they are likely not to increase immediately. This could lead to reduced farming activities (sowing and harvesting), resulting in lower crop yields. A broader food security crisis is on the horizon for Pakistan if the government fails to absorb some of the shock for the farmers as the Israel-Iran conflict drags on.

Additionally, the Oil and Gas Regulatory Authority (OGRA) has increased the price of Re-Gasified Liquefied Natural Gas (RLNG) by 22%. Pakistan’s RLNG is derived from the LNG imported from Qatar and the United Arab Emirates (UAE), responsible for about 99% of the country’s LNG imports. The power generation plants and textile industries in Pakistan consume most of the imported RLNG, where 21% of the country’s total power generation is contributed by the RLNG-fired plants and about 55% of Pakistan’s total exports are made up of textile products. The impacts on these sectors will translate into higher electricity costs for the locals and a significant volume of layoffs in the textile sector due to production shutdown, as manufacturers struggle to manage rising energy costs. A slower industrial production growth, coupled with lower crop yield, will negatively impact the projected GDP growth rate of 3% – 4% for FY26.

Bangladesh

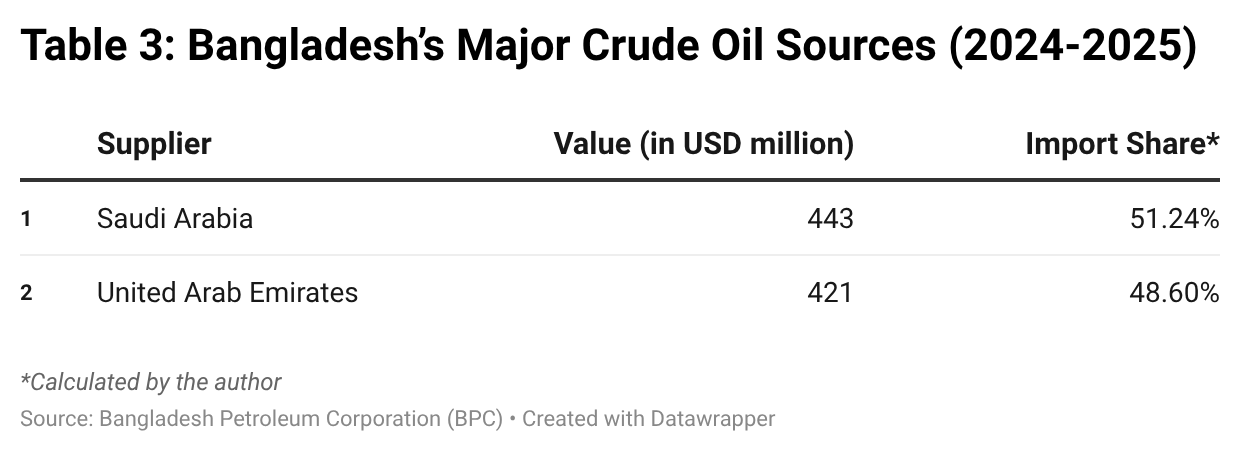

From Table 3, almost 100% of Bangladesh’s crude imports pass through the Strait of Hormuz, along with 71% of its LNG imports. Shortages in energy supplies and rising fuel prices have increased production costs for local garment factories and will likely remain in the long-run. Since Bangladesh’s Ready Made Garment (RMG) industry accounts for more than 80% of the country’s export income, it is highly likely that a loss of export competitiveness will undermine the country’s GDP growth.

In an attempt to stabilise the energy supply, Dhaka has ordered a cut in working hours for government employees and started rationing fuel. In addition, the government has implemented fuel subsidies to avoid oil price hikes. The reported tax-to-GDP ratio for Bangladesh is 6.7% in FY25. However, in the long run, expanding subsidies will further reduce Dhaka’s tax-to-GDP ratio in FY26.

Forecast

Short-term (Now - 3 months)

It is almost certain that energy-dependent industries in South Asia will continue to be affected by rising input costs and reduced demand for existing workers. This will likely translate into a price hike for finished products across sectors, reducing the region's export competitiveness.

It is highly likely that the temporary shutdown of SMEs in the region will persist despite the government’s effort to subsidise fuel.

It is likely that the agricultural sector will not see a sharp negative impact overall over the next three months but a significant burden on the farmers will likely cause civil unrest.

Medium-term (3 - 12 months)

It is likely that trade deficits and lower trade revenue will jeopardise planned investment programs in the region. This will delay agreed economic deals, impacting the countries’ targeted GDP growth and debt repayment schedules.

It is highly likely that agricultural output will be severely affected if the conflict lasts another 12 months. In this scenario, a food security crisis is almost certain in some South Asian countries (Sri Lanka, Nepal, Pakistan, and Bangladesh) due to depleted fertiliser and fuel stocks. The impact will be compounded if the Houthis block the Bab el-Mandab Strait.