AI Bubble Risk: Echoes of Dotcom?

By Tom Everill | December 2025

Summary

AI boom echoes Dotcom dynamics, but current valuations and index gains remain far below 1990s bubble levels.

Speculative capital is flowing into core infrastructure, raising risks of overbuild, weak monetisation, and reliance on scaling laws.

Market outcomes hinge on whether AI delivers sustained enterprise productivity, determining if this becomes a lasting tech cycle or a bubble.

Context

Wall Street has been abuzz of late with fears of an Artificial Intelligence (AI) bubble emerging in equity markets, reminiscent of the ‘Dotcom Bubble’ which famously burst in the early 2000s. These concerns are amplified by the concentration of US market gains among the seven largest technology companies, the Magnificent Seven, which now constitute almost 50% of the S&P 500 by market capitalisation.

In financial markets, a bubble occurs when asset prices rise rapidly, with optimism driving valuations far above intrinsic value, before a sharp decline. Many on Wall Street, including Michael Burry of The Big Short fame, who correctly predicted the 2008 Global Financial Crisis, believe we could be entering such a cycle.

‘Dotcom’ Comparisons

The post-2022 bull market, catalysed by AI, is increasingly drawing comparisons to the Dotcom Bubble, yet the data may suggest such comparisons are premature. Using the NASDAQ Composite as a barometer, the index rose roughly 700% from December 1995 to the Dotcom peak in March 2000. By contrast, from November 2022 (ChatGPT launch) to its most recent peak in October 2025, it rose only 125%, illustrating a much smaller price surge.

Another useful comparative metric is the forward price-to-earnings (P/E) ratio, referring to a company or index’s current stock price relative to its projected future earnings, offering a valuation measure based on expected, not historical, profitability. This metric tells a similar story with NASDAQ fwd P/E ratios roughly 79x at the Dotcom peak versus around 25x today. While this does not rule out a bubble, it suggests there is room before realistic comparisons to Dotcom.

Implications and analysis

Similarities

Both the Dotcom and AI booms were driven by speculative capital chasing general-purpose technologies with broad productivity potential. In both instances, an abundance of capital financed major infrastructure buildouts: fibre-optic and servers during Dotcom; GPUs, data centres and energy infrastructure for AI. As such, both cycles saw a high concentration of gains among the companies providing this foundational infrastructure: Cisco, AOL and telecom operators during Dotcom; Nvidia, Broadcom and hyperscalers / model developers in the AI-era, while investment optimism focused on speculative downstream applications.

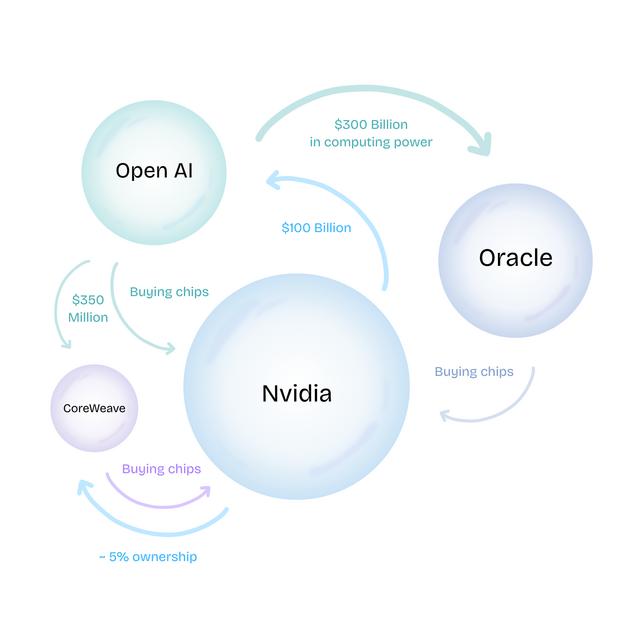

Both eras saw low barriers to startup formation, producing potentially frothy valuations: anyone with HTML, a domain and an idea could raise seed capital in the Dotcom era; today, anyone fine-tuning a model or wrapping an API can get funded. Vendor financing, where firms credit customers to purchase their products, today mirrors Dotcom. Today, foundation model developers and hyperscalers transact compute for equity (see recent OpenAI deals with Nvidia and AMD). In the Dotcom era, telecom equipment companies, like Lucent Technologies, which at one point saw USD 15b in vendor financing with only 300m in operating cash flow, transacted similarly.

Differences

However, there are differences between the eras. For example, Dotcom saw far more growth driven by IPOs and pre-revenue companies, while AI sees true revenue in hyperscalers and application-layer companies in the Magnificent Seven, such as Google and Meta. However, much of the latter’s revenue remains tied to ads or other non-AI streams. Furthermore, AI growth is constrained by physical limits: energy availability, chip manufacturing bottlenecks, and rare earth supply chains, unlike Dotcom, which was constrained only by user growth.

Another difference is how each technology scales. AI Scaling Laws suggest that increased compute, data, and parameters improve performance, contrasting the scaling-up of early internet infrastructure, which did not incur implicit product improvements. Additionally, AI presents immediate enterprise productivity opportunities rather than being purely consumer-driven like the Dotcom was initially.

Macroeconomic Factors

The Dotcom cycle occurred under higher interest rates (5 to 6.5%), tightening into 2000, contributing to the subsequent crash, whereas AI began under near-zero post-pandemic rates before hikes in 2023-24, meaning tightening came mid-cycle, rather than after speculative excess had peaked.

Liquidity sources and availability also differ: Dotcom capital flowed from organic growth and foreign investment, while AI growth follows pandemic-era fiscal and monetary stimulus. As a result, the abundance of policy-driven capital today may force deployment ahead of fundamentals, increasing the risk that lower-quality investments absorb excess liquidity. However, fewer IPOs mean capital is flowing mostly to established firms, perhaps reducing the risk of misallocation.

Bubble Burst Scenarios

Several dynamics could trigger a crash in today’s AI-driven markets. A core risk is infrastructure overbuild, with trillions flowing into data centres, chips and energy capacity ahead of sustainable demand, echoing the Dotcom-era fibre deployment that outpaced usage and left major carriers bankrupt with stranded assets.

This risk is compounded by the possibility that current AI architectures, particularly large transformer-based models, prove transitional, with potential alternative architecture breakthroughs rendering today’s capacity obsolete before achieving full return on investment. Additionally, Scaling Laws may face upper limits, either due to diminishing performance gains from parameter expansion, a lack of new high-quality data, or physical resource restraints. As investor expectations appear largely informed by the continuation of these scaling laws, a plateau would sharply reprice expectations in the short to medium term.

Another major vulnerability lies in monetisation. According to the FT, in the first half of 2025, OpenAI took in a reported USD 4.3b in revenue, while incurring operating losses of roughly USD 7.8b, indicating subscriptions and API usage are insufficient to cover costs. If revenue generated by AI applications fails to justify the vast capital expenditure required to train and deploy large models in the medium-term, valuations may decline sharply. Circular financing between hyperscalers and AI companies could amplify risk by distorting valuations, similar to Dotcom feedback loops.

Finally, geopolitical and regulatory shocks present meaningful downside risk. Export controls, US-China tech tensions, environmental policy, antitrust actions or restrictions on foundation model deployment could materially impair growth trajectories.

Forecast

Short-term (Now - 3 months)

AI markets likely remain elevated, driven by continued infrastructure investment and hyperscaler earnings.

Volatile responses to geopolitical, economic or other shocks are likely given underlying valuation concerns.

Medium-term (3-12 months)

If monetisation continues to lag → pressure increases on loss-making AI companies.

More defensive sectors like healthcare and staples are likely to see relative gains versus tech.

Realistic possibility for market repricing of tech stocks based on realised economic impact as exuberance wanes.

Long-term (>1 year)

If infrastructure exceeds demand or scaling laws plateau → market crash / large correction is a realistic possibility.

If scaling laws hold → enduring value likely remains in chips, data centres, etc.

Trajectory depends on adoption as a general-purpose technology and enterprise revenue growth across sectors.