Gulf Aviation’s Struggle During Regional Turbulence

By Trishnakhi Parashar | 8 July 2026

Summary

The Iran-Israel-USA war has shaken the Gulf aviation sector, putting immense pressure on operational efficiency and increasing uncertainty.

Airspace closures, flight cancellations, the requirement for longer routes, and higher fuel prices have cost Gulf carriers billions, weakening revenue growth and financial performance across the sector.

Gulf airlines entered 2025-26 profitably and maintained stable financial performance, demonstrating resilience amid geopolitical turbulence.

Context

Over the past decade, the Gulf Cooperation Council (GCC) states have transformed into one of the most important aviation hubs, connecting Europe, Asia, and Africa through world-class airport infrastructure and extensive airline networks. Nevertheless, the Middle East aviation landscape has been significantly upended by the outbreak of the Iran-Israel-USA war. Before the conflict, carriers in the GCC were coming off strong financial and operational performance; however, the escalation of the war shattered this momentum.

The operational disruptions were immediately reflected in flight schedules. According to aviation industry assessments, airlines cancelled more than 20,000 flights during the early phase of the conflict. Under normal conditions, the cancellation rates across the region typically remain below 2%, however, these rates rose above 65% during peak disruption. Particularly in Bahrain, flight cancellations reached a staggering rate of 96.67%. Moreover, the availability of seats also decreased as airlines temporarily suspended services on several international routes. Higher fuel prices emerged as another major challenge, with Brent crude oil prices surging above USD 100 per barrel. Simultaneously, airlines were forced to reroute flights around conflict zones, resulting in longer flight paths, greater fuel burn, and higher operating costs.

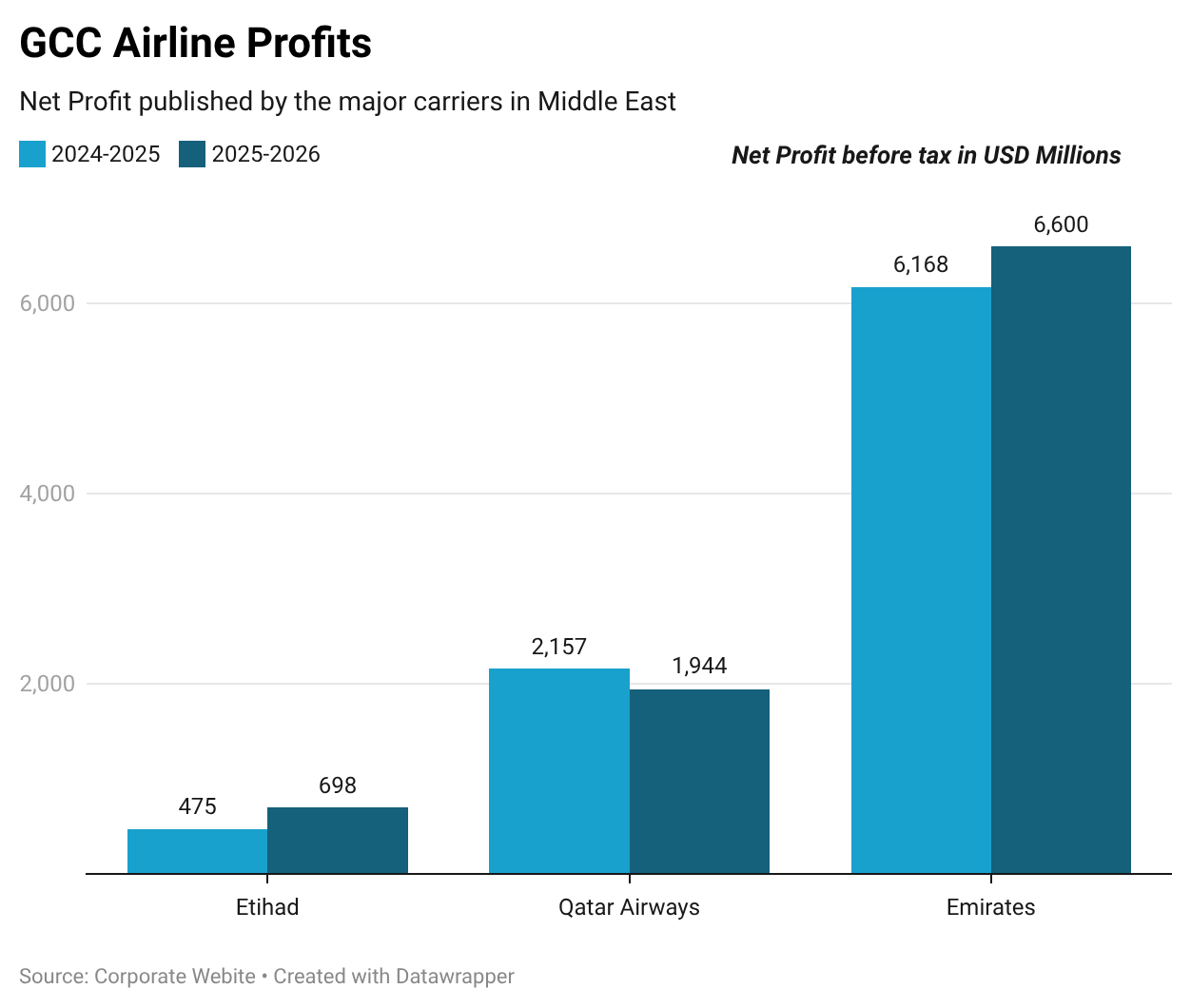

Recently, major Gulf airlines have released their financial year 2025-26 annual reports, revealing a broadly resilient period in the history of Middle Eastern aviation. Emirates reported a profit before tax of approximately USD 6.6 b, Qatar Airways achieved profits of almost USD 2 b, while Etihad Airways secured more than USD 690 m. Even low-cost carriers such as Air Arabia, which experienced multiple flight suspensions due to the crisis, reported solid operational performance by maintaining profitability despite a 22% decline in net worth and a 5% drop in passenger numbers in Q1 2026. Notably, the Gulf aviation sector experienced a profit squeeze rather than a sector-wide loss, demonstrating its underlying buoyancy while accentuating the strategic importance of aviation to the region. Collectively, these results cemented the Gulf’s position as one of the world’s most profitable aviation markets.

Implications

Regional tensions have exposed the geographical fragility embedded within the Gulf aviation sector. The war led to temporary airspace closures and disruptions across the region. Yet, the Gulf remains home to some of the world’s busiest international airports, and Gulf states continue to position themselves as global aviation and logistics hubs. Consequently, in response, Gulf authorities intensified diplomatic efforts to protect regional security and stability. The recent US-Iran agreement has reduced immediate escalation risk to some extent; however, the crisis reinforced the fact that sustained aviation growth depends not only on infrastructure and investment, but also on a stable geopolitical environment and regional cooperation.

The war fundamentally remapped existing aviation routes throughout the region. However, after three months of uncertainty, airlines did not merely endure the crisis; they gradually adapted through operational restructuring. Gulf airlines continue to handle long-haul traffic but have systematically reduced and restructured their operations. Airlines have not fundamentally altered their growth ambitions but seem to be prioritising operational continuity and network resilience at this moment. By mid-June, most airlines had restored more than 80% of their pre-war level of operations. In the air cargo segment, passenger flight reductions removed substantial belly-hold capacity during the war, forcing dedicated freighter aircraft to assume a greater role in maintaining trade flows. At the peak of the disruption, several Gulf-linked cargo routes experienced capacity decline up to 49% compared with the previous week. As of June, the picture is gradually stabilising as operations recover and airspace access improves.

Throughout the war period, security implications were a major concern for the aviation sector. Several major airports have sustained damage due to missile and drone strikes, raising red flags for the safety of passengers, airport workers, aircraft, and airport infrastructure. Even during the ongoing negotiations with the US, Iran reportedly launched a retaliatory strike targeting Kuwait International Airport, killing one person and injuring many others. Following this, Kuwait temporarily suspended air traffic and diverted flights. Such incidents highlight the growing vulnerability of the civilian aviation sector.

The overall economic toll has been significant. The airlines were operating steadily and remained profitable while the crisis unfolded, with years of strong financial performance proving crucial in cushioning the war impact. According to the International Air Transport Association’s (IATA) latest financial outlook for the global airline industry, Middle East airlines are expected to record a collective loss of USD 4.3 b in 2026. Beyond direct revenue losses, the conflict substantially increased operating costs through longer flight routings, higher fuel consumption, insurance premiums, and crew maintenance expenses.

Due to the crisis, forward bookings reportedly weakened while cancellation rates climbed, resulting in a decline of international visitors across the Middle East. IATA also projects that profit per passenger will fall sharply from USD 31.5 last year to a loss of USD 21.40. However, global passenger demand remained resilient, in spite of cost increases.

Once the immediate crisis eased, the response was a recovery and restructuring rather than a return to the normal phase. Several airlines introduced flexible booking policies, including complimentary rebooking and refund waivers to rebuild forward demand. Emirates plans to attract passengers through different incentives, whereas many airlines have reduced their loyalty incentives. Qatar Airways has responded with drastic cost-cutting measures, including the suspension of employee bonus payments, while Etihad accelerated its long-term fleet expansion by ordering additional widebody aircraft.

Juke Schweizer/Wikimedia

Forecast

Short-term (Now - 3 months)

Except for a handful of airlines, most Gulf carriers have resumed over 80% of their normal operations and are most likely to maintain stable operational performance in the near term.

Although crude oil prices have fallen by 38% from the wartime, airfare costs are likely to remain elevated due to a war premium.

Despite the end of hostilities, passenger demand remains below pre-war projections, as travellers are likely to consider geopolitical uncertainties into their booking decisions.

Medium-term (3 - 12 months)

There is a realistic possibility that premium Gulf airlines may restore earnings momentum in the medium term; however, such a recovery is unlikely to be sector-wide as low-cost carriers are expected to require a longer adjustment period.

Long-term (>1 year)

If the US-Iran agreement holds, Gulf aviation is likely to emerge from the crisis with profitability; however, the post-crisis recovery and competitive pressure may lead to strategic partnerships or government support, particularly among smaller airlines, is a realistic possibility.