From Oil Crisis to Currency Crisis: The Knock-On Shock in Emerging Markets

By David Yang | 8 June 2026

Musabbir Uddin/Wikimedia

Summary

The surge in energy import prices due to the closure of the Strait of Hormuz has caused the currencies of many emerging markets (EMs) to depreciate sharply against the USD.

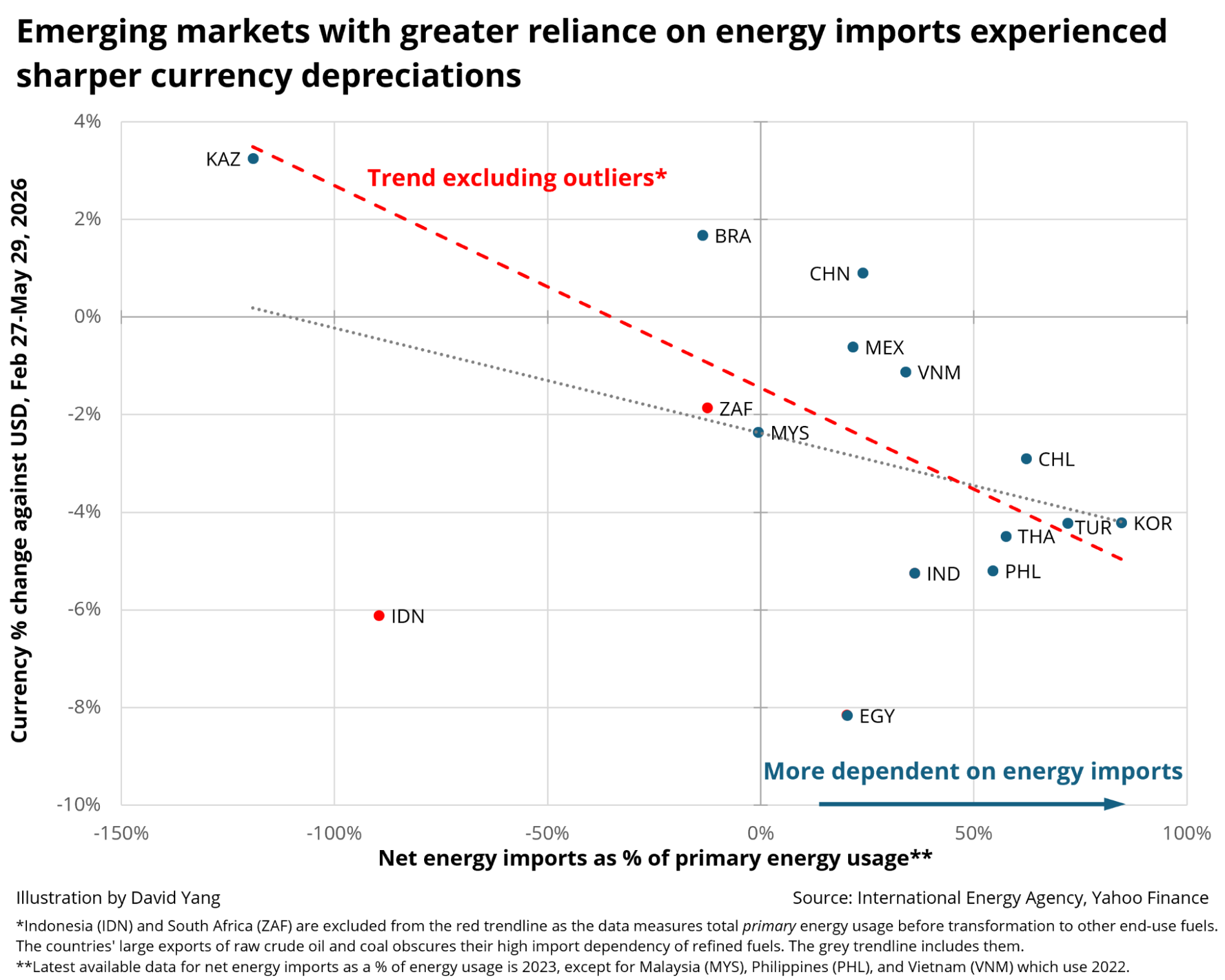

Countries with greater dependence on energy imports have experienced steeper declines, tightening financial conditions just as recession risk rises. Asian EMs are particularly impacted due to their greater reliance on imports that transit the Strait of Hormuz.

A repeat of the 1997 Asian Financial Crisis is highly unlikely, as the depreciation in currencies so far is a necessary but painful balance of payments adjustment needed to keep EMs solvent. However, government efforts to defend their currencies, like Turkey’s, are unsustainable and likely to only exacerbate future balance of payment issues.

Context

The conflict in the Persian Gulf has caused an acute global supply shortage of oil and refined petroleum products. However, on top of the physical crisis that affects all countries, emerging economies are doubly hit by weakening currencies, which further increase energy costs and tighten financial conditions.

Oil is priced in dollars, meaning that when prices rise, countries will sell their domestic currency to buy the dollars needed to offset the increased energy costs. This depreciates their currencies, further raising the price of energy imports in domestic terms. With many emerging markets (EMs) being highly dependent on fossil fuels that transit the Strait of Hormuz, EM currencies have been sharply hit by the Strait closure.

Implications

Beyond higher energy import costs, the oil shock poses financial risks to EMs. To attract foreign lenders, EMs issue much of their government and corporate debt in dollars. This makes domestic currency depreciation equivalent to a tightening of borrowing conditions: borrowers will have to pay more in domestic terms to service the same debt. This puts further pressure on private demand and investment, and constrains governments’ ability to provide a fiscal cushion to households and businesses.

This has the potential to cause a vicious cycle for net energy importers such as India, South Korea, and the Philippines. The rise in energy prices and depreciating currency both squeeze households and businesses. Governments have and will likely continue to spend on fuel subsidies and tax cuts to protect them, which, combined with more expensive USD-denominated debt, worsens the government’s fiscal position. Bond investors, already raising yields to compensate for higher inflation from the energy crisis, have further reason to demand higher yields on more unsustainable borrowing or to stop lending to emerging markets altogether, deepening the currency and debt spiral.

If the energy crisis persists, it poses a serious risk to EM governments, particularly in Asia, which are highly dependent on Middle Eastern energy supplies. However, the painful currency depreciation resulting from the surge in energy costs is precisely the macroeconomic adjustment needed to stabilise countries’ balance of payments and avoid a repeat of the 1997 Asian Financial Crisis.

To avoid the depreciation cycle, some governments have turned to defending their currency by selling foreign reserves and buying domestic currency to prop up its value, as Turkey has done most notably. However, the persistent depreciative pressure of the energy shock means that foreign exchange (FX) intervention can last only as long as the country has reserves to sell, and creates a balance-of-payments crisis-in-waiting.

The oil shock raises economy-wide inflation more in energy-import-dependent emerging markets that spend more on basic fuel and food than in advanced economies. Preventing the currency from depreciating means that, as domestic goods prices rise more quickly than the price of imported goods, EM consumers are incentivised to import more while exporters become less competitive from higher input costs, widening the current account deficit.

With the energy crisis depriving governments of foreign debt funding, governments are balancing the wider current account deficit by draining their finite reserves. When reserves inevitably run out, the balance of payments will adjust toward equilibrium through a sharp, chaotic currency depreciation so that net imports fall. This worsens inflation and risks a banking crisis akin to that of 1997.

In contrast, allowing the currency to depreciate naturally equilibrates the balance of payments. Depreciation makes imports more expensive and exports more competitive, counteracting the inflation effect, and narrows the current account deficit. This gradually reduces depreciative pressures, allowing households and businesses to adjust. A chaotic depreciation will only exacerbate the developing economic crisis and further stoke political unrest over fuel prices and wider inflation, such as those in the Philippines, India, and across Africa.

Forecast

Short-term (Now - 3 months)

If the Strait of Hormuz remains closed, EM currencies are highly likely to continue depreciating against the dollar as their economies adjust to the energy shock.

Without restoration of Middle Eastern supply flows, global fuel stocks will highly likely fall below “critical levels” during Q3 2026, likely unleashing a second sharp price increase.

Medium-term (3 - 12 months)

If the Strait closure persists through 2026, emerging economies that have used up much of their energy stockpiles and already started rationing will likely see demand destruction and tip toward recession.

Protests sparked by the economic hardship, but also growing into wider political discontent, are very likely to grow the longer the crisis wears on.

Long-term (>1 year)

Even a short-lived crisis will likely push emerging markets to diversify energy types away from fossil fuels and sources away from the Middle East. Moves like India’s zoning changes to expand nuclear power generation are likely to be seen across vulnerable EMs with a push for domestically generated power.