Can US drillers plug the global oil gap?

By David Yang | 18 May 2026

Summary

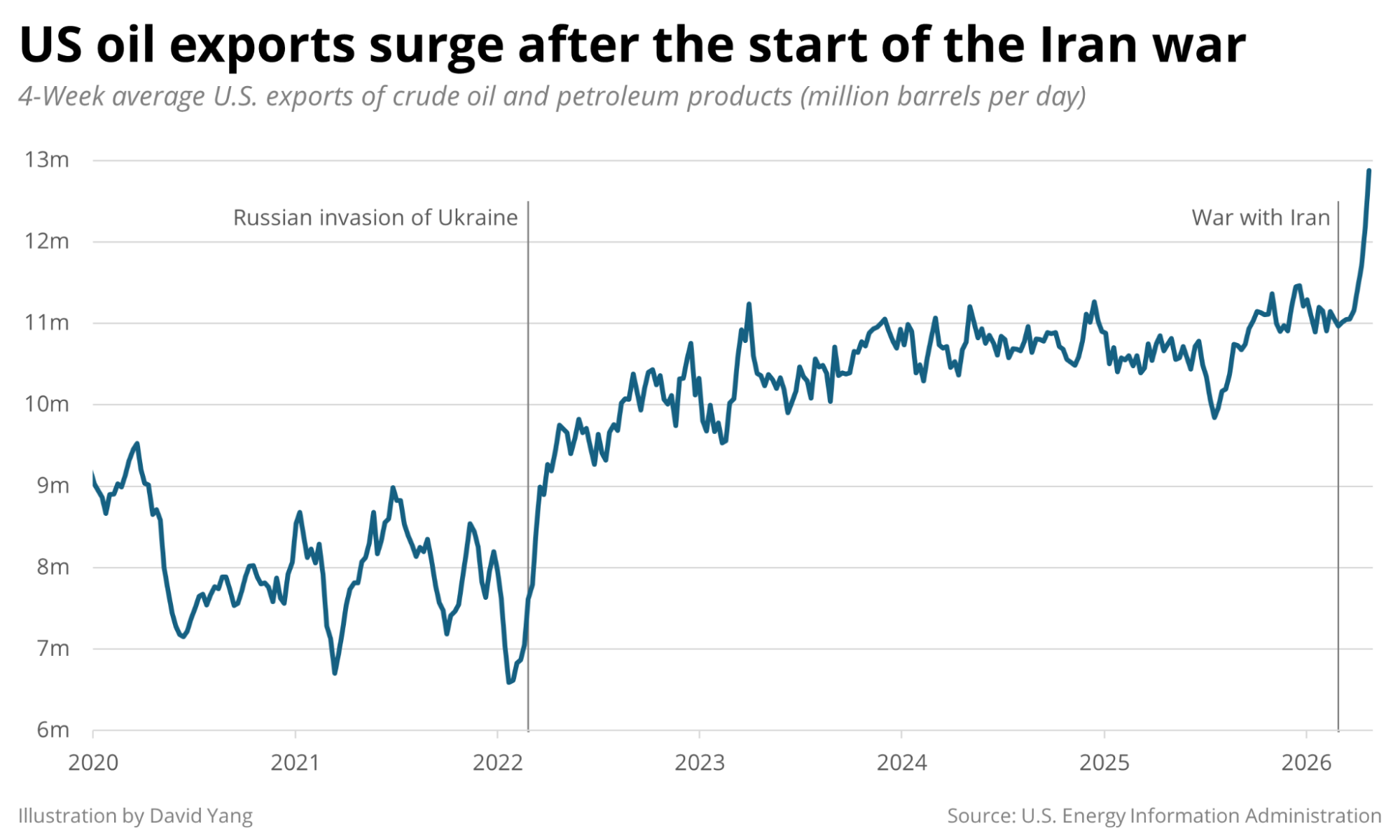

As the Strait of Hormuz remains closed, choking off at least 13m barrels per day (bpd) of oil shipments, the United States’ (US) energy exports have surged to all-time highs as the world seeks alternative supplies.

The US’ status as the world’s largest producer of crude oil has highlighted the potential of increased production from shale drillers in the Permian Basin, the US’ main oil plot, to relieve global supply shortages.

However, it is unlikely that US oil producers will meaningfully increase production in the short term as the oil price outlook remains highly volatile due to geopolitical uncertainty, and infrastructure constraints limit a rapid ramp-up.

Context

As the conflict between the US and Iran enters its third month, the Strait of Hormuz remains largely closed, and the global energy crisis deepens. The International Energy Agency estimates that at least 13 million bpd of oil shipments have been cut off from global supply, leading to energy rationing and skyrocketing prices.

The US, the world’s largest crude oil producer at 13.6m bpd in 2025, has emerged as a key alternative source, with an estimated 172 oil tankers en route to the US Gulf Coast to pick up US exports as of April 12. Exports of crude oil and petroleum products have already surged by 1m bpd since the onset of the war, as US producers can receive high prices on international markets. However, without an increase in total oil production, domestic US energy costs will increase, a particular political pain point.

Implications

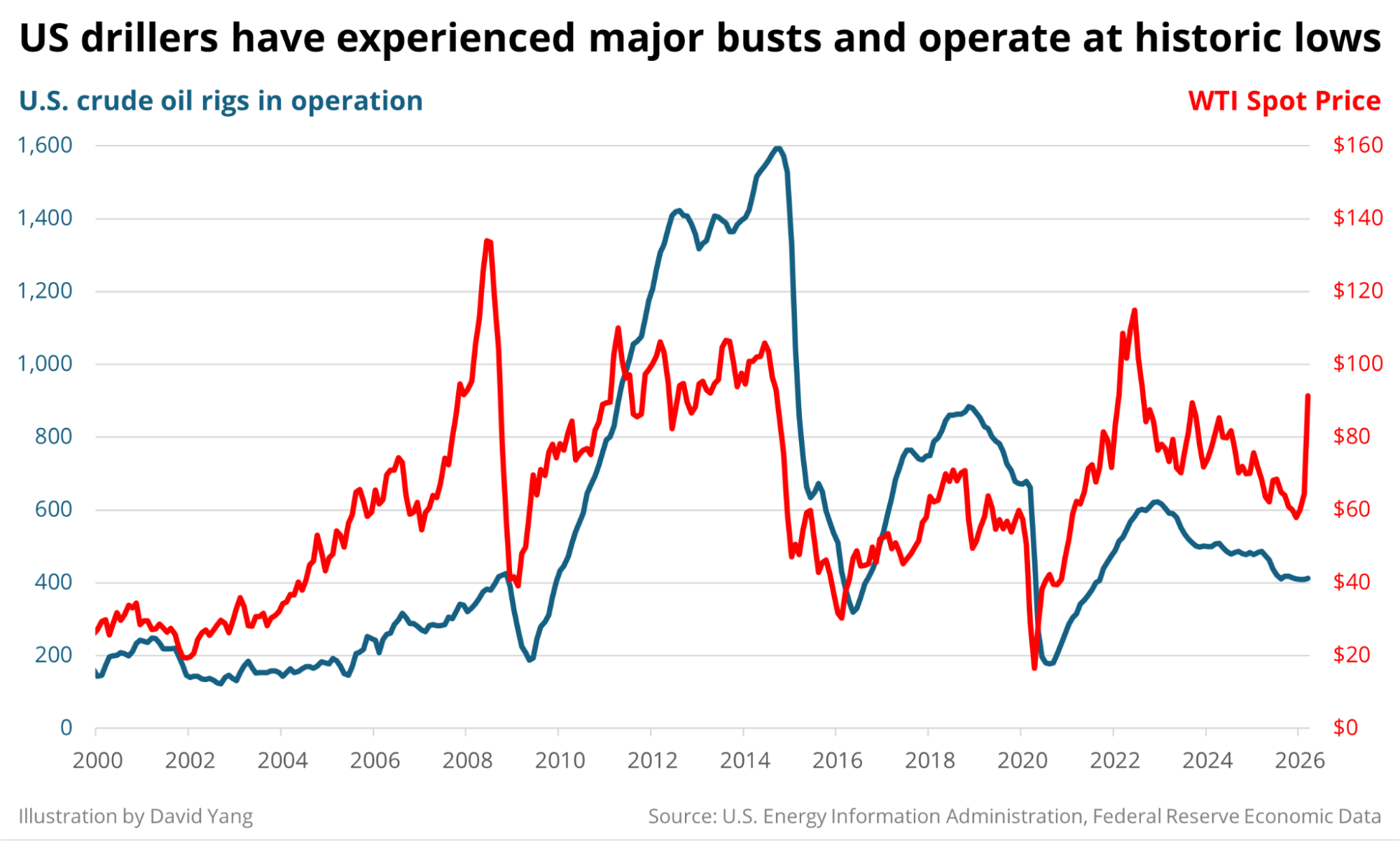

Despite the Trump Administration's urging of US oil drillers to ramp up production amid high global prices, oil executives remain reluctant to rapidly expand output. Uncertainty over long-term oil prices and midstream infrastructure constraints make it highly unlikely that US shale drillers will be able to meaningfully narrow the global supply deficit in the short-term. Unlike OPEC members with large state-owned oil companies that maintain spare production capacity, US shale oil drillers are small private companies that profit maximise by utilising full capacity.

A Dallas Fed survey of energy firms from the first quarter of 2026 found that exploration and production firms needed consistent Western Texas Intermediate (WTI, the main American benchmark) oil prices of USD 67 per barrel to profitably drill a new well. Prior to the war, WTI hovered below USD 60. Although WTI prices have soared over 50% since the start of the conflict, they remain highly volatile, ranging between USD 84 to USD 113.

US drillers will likely be hesitant to invest in new rigs due to the time necessary to become operational. Put against the historic context, the US drillers that drove the shale boom have been burned multiple times by over-aggressive production expansion that led to supply gluts and depressed prices. Since then, the financial backers behind shale drillers have avoided aggressive expansion, instead distributing profits to shareholders. Exxon and Chevron have maintained their strategy prioritising cash flow growth over production. Rig counts have steadily declined since the start of 2023, and the Dallas Fed Energy Survey reported that 53% of exploration and production firms had no change in the number of wells they expected to drill, despite elevated prices.

Even if drillers can be confident of persistently high prices, there is an infrastructure constraint on expanding production now. Shale oil extraction also draws natural gas that must be piped away, as environmental regulations ban flaring or direct releases into the atmosphere in most cases. However, Permian Basin gas takeaway pipelines are already at maximum capacity, and major pipeline projects are set to come online in November at the earliest. Thus, increased oil production could only start to contribute to supply in half a year, as opposed to being a short-term solution to the crisis.

Lastly, other state oil producers with spare capacity will not hold back for US drillers. The United Arab Emirates’ decision to leave the Organisation of Petroleum Exporting Countries (OPEC) was out of frustration with the bloc’s output limits, and OPEC itself has continued to signal that it will raise production once the conflict is resolved.

In the face of these headwinds, the Trump Administration has offered some incentives for increased production. The Environmental Protection Agency has posted guidance on specific conditions where flaring is permitted, while the administration has offered contracts to US producers to refill the Strategic Petroleum Reserve for some long-term guaranteed demand. Despite the incentives, however, price uncertainty and foreign competition make the prospect of an American shale revival highly unlikely.

Forecast

Short-term (Now - 3 months)

Continued uncertainty over the resolution of the conflict and the closure of the Strait of Hormuz will highly likely dissuade most shale drillers from immediate output expansion in H1 2026. Firms have little incentive to risk capital when they can reap profits now.

Medium-term (3 - 12 months)

If the crisis persists and oil prices remain high, a moderate increase in supply is a realistic possibility once gas takeaway infrastructure comes online. However, this is highly path-dependent on the conflict.

The UAE’s departure from OPEC is unlikely to see a massive increase in global oil supply post-conflict from the baseline, as both OPEC and the UAE will likely be aligned on increasing output to fill shortages.

Long-term (>1 year)

There is a remote chance of an increase in US oil supply comparable to the previous shale boom, as shareholders are careful to avoid repeating previous bust cycles. The UAE’s commitment to higher production means long-term oil prices are unlikely to remain persistently above US drillers’ break-evens.

Any production increase is highly likely to be gradual and restrained, particularly as long-term global energy demand rotates away from oil to more shock-resilient sources.